Integrated report 2019

Exxaro Resources Limited

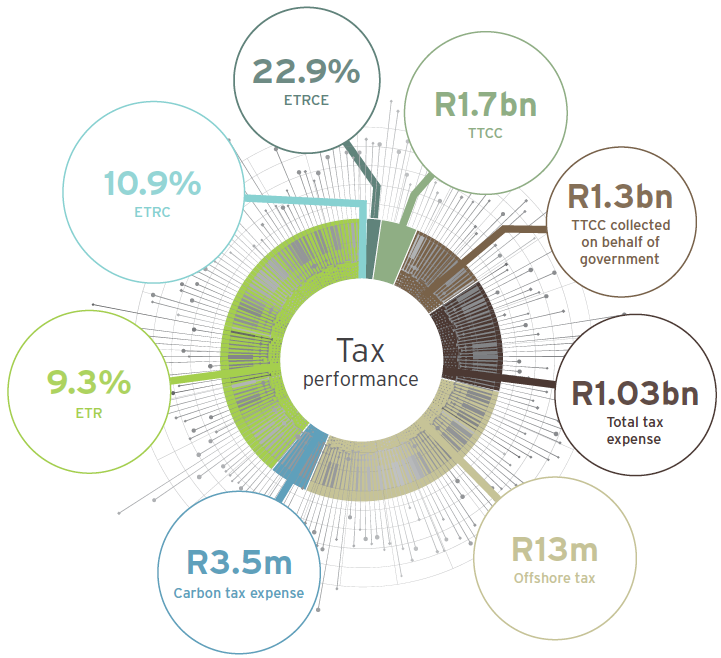

Tax report for the year ended 31 December 2019

Relevant tax matters are identified by considering issues identified through:

These are prioritised based on inherent risk and predetermined risk appetite against the likelihood of the matter arising and its impact on value creation. Only the top five material tax risks and opportunities are discussed in this report.

|

Ranking |

Risk |

Context |

Strategic treatment |

||||

|

1 |

Diesel-rebate audits |

Uncertainty of the SARS compliance requirements relating to diesel rebates threatens non-payment by SARS of diesel rebates Audits by SARS are prolonged for unreasonable periods |

Continuous engagement with SARS to understand their requirements Meetings with new service providers to assist with updating logbooks to meet SARS requirements |

||||

|

2 |

Understatement penalties |

The scope of the definition of "prejudice" to SARS in the Tax Administration Act, 2011 (Act 28 of 2011) is very wide, leaving little room for genuine inadvertent errors or any disclosure errors Understatement penalties for the taxpayer are severe, even if SARS suffered no financial loss due to taxpayer disclosure errors SARS penalties imposed due to incorrect tax returns filed as a result of incorrect Annual financial statement (AFS) disclosures SARS penalties imposed for late submission due to the late issuance of AFS |

The group tax manager performs detailed reviews of submissions to SARS instead of high-level reviews Automation of the tax return pack assists in ensuring errors are not made Tax consultants are more involved in the day-to-day business operations to ensure a better understanding of the business to enable tax consultants to question incorrect inputs into the tax return packs from business units AFS are completed in terms of the latest international financial reporting standards and reviewed by various levels of senior management and directors of the legal entity Timeous issuance of AFS by strict adherence to the corporate financial reporting calendar |

||||

|

3 |

Exxaro group companies are not able to obtain tax clearance certificates (TCCs) |

Exxaro companies cannot conduct business and therefor suffers cash flow constraints without TCCs State-owned entities use different government systems to check a supplier's tax status and not the SARS system – these systems are not always aligned, so the supplier incorrectly appears to be non-compliant Diesel-rebate audits are not finalised resulting in the SARS VAT system showing short payments. The absence of a separate SARS diesel-rebate e-filing system leads to constant tax-compliant status failures |

Exxaro maintains good relationships with dedicated SARS relationship officers and SARS Large Business Centre reacts promptly when there appear to be system failures The Exxaro tax team will employ another team member in 2020 to alleviate the tax-compliance burden Exxaro is also investigating alternative systems to comply with SARS requirements for diesel refunds (refer to point 1 above) |

||||

|

4 |

Disposals and acquisitions of investments |

Understanding the tax effects of complex transactions |

Exxaro's tax function signs off submissions to the investment review committee and executive committee's decisions on capital spent Using expert legal advice for complex restructuring transactions |

||||

|

5 |

Document retention |

Exxaro's policy is to retain documents for a period of seven years in line with the Companies Act, 2008 (Act 71 of 2008) but SARS sometimes requests information for periods exceeding seven years Inability to comply with SARS requests can lead to negative tax adjustments |

Exxaro strives to adhere to SARS requirements for tax submissions to ensure return prescription periods do not exceed the seven-year period for document retention |

| TTCC | Total tax cash contribution. |

| ETR | Effective tax rate. |

| ETRC | Effective tax rate — continuing operations. |

| ETRCE | Effective tax rate — continuing operations — excluding equity-accounted investments. |