NOTES TO THE REVIEWED CONDENSED GROUP ANNUAL FINANCIAL STATEMENTS

1. CORPORATE BACKGROUND

Exxaro, a public company incorporated in South Africa, is a diversified resources group with interests in the coal (controlled and non-controlled), energy (controlled and non-controlled), TiO2 (non-controlled) and ferrous (controlled and non-controlled) markets. These reviewed condensed group annual financial statements as at and for the year ended 31 December 2020 (condensed annual financial statements) comprise the company and its subsidiaries (together referred to as the group) and the group's interest in associates and joint ventures.

2. BASIS OF PREPARATION

| 2.1 | Statement of compliance | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

The condensed annual financial statements have been prepared in accordance with the requirements of the JSE Listings Requirements for preliminary reports and the requirements of the Companies Act of South Africa. The Listings Requirements require preliminary reports to be prepared in accordance with the framework concepts and the measurement and recognition requirements of IFRS (as issued by the IASB), the SAICA Financial Reporting Guides (as issued by the Accounting Practices Committee) and Financial Pronouncements (as issued by the Financial Reporting Standards Council). As a minimum, preliminary reports must contain the information required by IAS 34 Interim Financial Reporting. The condensed annual financial statements have been prepared under the supervision of Mr PA Koppeschaar CA(SA), SAICA registration number: 00038621. The condensed annual financial statements should be read in conjunction with the group annual financial statements as at and for the year ended 31 December 2019, which have been prepared in accordance with IFRS. The condensed annual financial statements have been prepared on the historical cost basis, except for financial instruments, share-based payments and biological assets, which are measured at fair value. The condensed annual financial statements of the Exxaro group were authorised for issue by the board of directors on 16 March 2021. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2.2 | Judgements and estimates | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Management made judgements, estimates and assumptions that affect the application of accounting policies and the reported amounts of assets, liabilities, income and expenses. Actual results may differ from these estimates. The significant judgements and the key source of estimation uncertainty were similar to those applied to the group annual financial statements as at and for the year ended 31 December 2019. In addition, certain new judgements, estimates and assumptions relating to the business combination have been applied as detailed in note 4. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2.3 | Re-presentation of comparative information | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

The condensed group statement of comprehensive income (and related notes) for the year ended 31 December 2019 and the condensed group statement of financial position (and related notes) at 31 December 2019 have been re-presented as a result of the investment in Black Mountain no longer meeting the criteria to be classified as a non-current asset held-for-sale and a discontinued operation due to the suspension of the sales process in December 2020. The impact of the re-presentation of 2019 was as follows:

|

3. ACCOUNTING POLICIES AND OTHER COMPLIANCE MATTERS

The accounting policies applied in the preparation of the condensed annual financial statements are consistent with those of the group annual financial statements as at and for the year ended 31 December 2019. A number of new or amended standards became effective for the current reporting period, however, the group did not have to change its accounting policies nor make retrospective adjustments as a result of adopting these standards. In addition the group has adopted hedge accounting as described further in note 23.2.1 following on the Cennergi business combination.

| 3.1 | Impact of new, amended or revised standards issued but not yet effective |

|

New accounting standards, amendments to accounting standards and interpretations issued which are relevant to the group, but not yet effective on 31 December 2020, have not been early adopted. The group continuously evaluates the impact of these standards and amendments and does not anticipate that there will be a material impact. |

|

| 3.2 | Carbon tax |

|

Following on the enactment of the Carbon Tax Act No 15 of 2019, as amended, Exxaro has licensed each of its emissions generating facilities with SARS, of which two subsidiaries only received their licenses in February 2021. The group has accrued R5.4 million (2019: R3.4 million) for Carbon tax which is payable on 29 July 2021. |

|

| 3.3 | Impact of COVID-19 on financial reporting |

|

The COVID-19 pandemic developed rapidly in 2020, not only in the world, but South Africa specifically has seen a significant number of infections being reported. Measures to prevent transmission of the virus included limiting the movement of people, restricting flights and other travel, temporarily closing businesses and schools and cancelling of public events. This had an immediate impact on the economy of South Africa. Measures taken to contain the virus affected economic activity, which in turn had implications on the financial reporting. The following key areas of financial reporting required specific attention for the year ended 31 December 2020: Revenue recognition Changes to terms of customer contracts and business practices during COVID-19 were evaluated and found not to influence the recognition of revenue. Inventory Inventory has been evaluated and written down to the lower of cost and net realisable value. An amount of R9 million on the write-down of inventory from cost to net realisable value has been recognised for 2020. Impairment of non-financial assets Impairment testing was based on the latest budgets which incorporated changes in parameters and economic outlooks revised for the effects of COVID-19. As at 31 December 2020, the investment in Insect Technology was fully impaired. Allowances for expected credit losses (ECLs) When assessing the amount to be recognised for ECLs, management considered the impact that COVID-19 had on the risk of default as well as the expected loss rates. The trade and other receivables are categorised into the following categories corporate, public sector as well as small and medium enterprises. Where additional risk was identified the credit ratings of each counterparty were reviewed and adjusted accordingly with a corresponding adjustment to the PD and LGD rates. Although these adjustments resulted in higher ECL multipliers the ECL amount recognised for 2020 was not significant as the trade and other receivables outstanding balance was 14% lower than 2019 and certain of the long outstanding other receivable debtors settled their debt during the year. Taxation Exxaro benefited from the following tax relief measures announced:

Going concern assessment The going concern assessment was based on the latest budgets that incorporated changes in parameters and economic outlooks revised for the effects of COVID-19. Additional sensitivity analysis was performed as part of stress testing the going concern assumption. Exxaro also prudently increased its available borrowing facilities. The additional facility was available from 1 July 2020. |

4. BUSINESS COMBINATION: ACQUISITION OF CONTROLLING INTEREST IN CENNERGI

| 4.1 | Overview of Cennergi | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

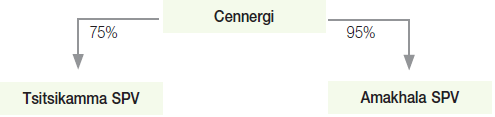

Exxaro and Tata Power, through its wholly owned subsidiary Khopoli, formed a 50:50 JV to create Cennergi in March 2012. Exxaro has recognised its existing 50% interest in the JV as an equity-accounted investment. Cennergi is a company established and registered in South Africa operating in the renewable energy sector. Its business is the investigation of feasibility, development, ownership, operation, maintenance, acquisition and management of renewable energy projects in certain permitted territories. Cennergi owns two wind farms which were originally bid as part of Window 2 of the Department of Energy's Renewable Energy Independent Power Producer Procurement Programme (REIPPPP) namely:

Each of the wind farms has been set up in separate project companies (SPVs) of which Cennergi holds the controlling interest as illustrated in the diagram below:

Cennergi forms part of the energy reportable segment. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 4.2 | Overview of the transaction | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Tata Power decided to dispose of its 50% interest in Cennergi creating an opportunity for Exxaro to act on its ambitions of growing its presence in the energy sector, by acquiring the 50% interest owned by Khopoli. The acquisition contributes towards aligning the long-term environmental, sustainability, growth strategy and expansion of Exxaro into renewable energies and aligns the strategic intent of Exxaro of forming a second core business next to coal. Therefore, with effect from 1 April 2020, Exxaro acquired Khopoli's 50% share of the issued share capital of Cennergi, resulting in Exxaro obtaining sole control over Cennergi. The transaction has been accounted for as a business combination achieved in stages (step-up acquisition) in terms of IFRS 3 Business Combinations (IFRS 3). Given the existing relationship with Cennergi, the related cost associated with the acquisition of the remaining 50% interest was minimal, with an amount of R2.4 million being expensed through operating expenses. The fair value of the 100% controlling interest acquired and its attribution to the net identifiable assets acquired and resultant goodwill is summarised below:

The accounting for the acquisition of Cennergi in terms of IFRS 3 was provisionally reported on for the six-month period ended 30 June 2020. Subsequently, the following changes to the purchase price allocation were made:

The reviewed condensed group interim financial statements as at and for the six-month period ending 30 June 2021 will be re-presented for these changes. At 31 December 2020 the accounting for the acquisition of Cennergi has been concluded. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 4.2.1 | Purchase consideration for newly acquired 50% interest | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

The purchase consideration for the additional 50% interest acquired in Cennergi has been fully settled in cash. The purchase consideration represents the consideration transferred at its acquisition-date fair value. This is summarised into its components as follows:

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 4.2.2 | Fair value of pre-existing 50% interest | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

The pre-existing 50% interest in Cennergi forms part of the 100% controlling interest that Exxaro holds as of the acquisition date and is therefore fair valued immediately preceding the acquisition date. The gain resulting from remeasuring the pre-existing interest was recognised in profit or loss and is ultimately treated as a deemed disposal of the pre-existing interest. The deemed disposal and fair value recognition is summarised as follows:

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 4.2.3 | Goodwill | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Goodwill represents the residual value between the fair value of the 100% controlling interest acquired, the net identifiable assets recognised and non-controlling interests recognised. The value of goodwill is attributed to the value of other items at acquisition date which are not separately identifiable to achieve recognition as intangible assets. The goodwill recognised is attributed mainly to:

The goodwill is not deductible for tax purposes. An impairment assessment was performed on 31 December 2020 for the goodwill acquired. The assessment resulted in no impairment charge for the year. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 4.2.4 | Identifiable assets acquired and liabilities assumed | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

The fair value of the identifiable assets acquired and liabilities assumed of Cennergi as at the acquisition date are summarised as follows:

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 4.2.5 | Non-controlling interests | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

The arrangements in place with the minority shareholders of Tsitsikamma SPV and Amakhala SPV represent a fully vested share-based payment arrangements under IFRS 2. The arrangements are viewed as in substance share options with the minorities, as the minorities are not exposed to downside risk nor benefit, until such time that the underlying shareholder financing of the arrangements has been settled. For the purposes of the acquisition Cennergi, as the acquiree, has outstanding share-based payment transactions that Exxaro, as the acquirer, did not replace, cancel or exchange as part of the acquisition. The share-based payment transactions have vested and therefore the share-based payment transactions of Cennergi are accounted for as part of the non-controlling interests in the Cennergi group acquisition and are measured at their market-based measure in terms of IFRS 2 Share-based Payment (IFRS 2). |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 4.3 | Performance contribution to Exxaro’s results | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 4.4 | Key judgements, assumptions and estimates applied to the business combination transaction | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 4.4.1 | Fair values of material assets acquired | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

The following material assets were fair valued applying the following valuation techniques and key assumptions:

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 4.4.2 | Non-controlling interests | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Management view the share-based payment transactions with the BEE minority shareholders of the SPVs as in substance share options that are equity-settled in terms of IFRS 2. These options were not yet exercised at the acquisition date.

|

5. SEGMENTAL INFORMATION

Operating segments are reported in a manner consistent with the internal reporting provided to the chief operating decision maker, who is responsible for allocating resources and assessing performance of the reportable operating segments. The chief operating decision maker is the group executive committee. Segments reported are based on the group's different commodities and operations.

During the second half of 2020, the chief operating decision maker, in line with reporting trends and better disclosure, revised the allocation of corporate costs to the segments since emphasis is placed on controllable costs. Indirect corporate costs are no longer allocated between the different segments but now reported on a gross level in the other reportable segment. The comparative segmental information has been represented to reflect this change.

The segments, as described below, offer different goods and services, and are managed separately based on commodity, location and support function grouping. The group executive committee reviews internal management reports on these operating segments at least quarterly.

Coal

The coal reportable segment is split between commercial (Waterberg and Mpumalanga), tied and other operations. Commercial Mpumalanga operations include a 50% (2019: 50%) investment in Mafube (a joint venture with Anglo) and a 49% (2019: 49%) equity interest in Tumelo. The 10.26% (2019: 10.36%) effective equity interest in RBCT is included in the other coal operations. The coal operations produce thermal coal, metallurgical coal and SSCC.

The export revenue and related export cost items have been allocated between the coal reportable segments based on the origin of the initial coal production.

Energy

On 1 April 2020, Exxaro obtained 100% control over Cennergi (2019: 50% joint control) (refer note 4 for detail of the business combination). The energy reportable segment also includes an equity interest of 28.59% (2019: 28.59%) in LightApp, as well as an equity interest of 22% (2019: 22%) in GAM.

Ferrous

The ferrous reportable segment mainly comprises of the 20.62% (2019: 20.62%) equity interest in SIOC (located in the Northern Cape province) reported within the other ferrous reportable segment, as well as the FerroAlloys operation (referred to as Alloys). The Alloys operation manufactures ferrosilicon.

TiO2

The TiO2 reportable segment comprises a 10.26% (2019: 10.38%) equity interest in Tronox Holdings plc, which was classified as a non-current asset held-for-sale on 30 September 2017 (refer note 17), and a 26% (2019: 26%) equity interest in Tronox SA (both South African-based operations).

Other

The other reportable segment is split between the base metals and other reportable segments. The 26% (2019: 26%) equity interest in Black Mountain (located in the Northern Cape province) is included in the base metals reportable segment. The other reportable segment comprises an equity interest in Insect Technology of 25.85% (2019: 25.86%), the Ferroland agricultural operation and the corporate office which renders services to operations and other customers. The 15% (2019: 15%) equity interest in Curapipe was disposed of on 9 November 2020.

The following table presents a summary of the group's segmental information:

| Coal | ||||||||||

| Commercial | ||||||||||

| For the year ended 31 December 2020 (Reviewed) | Waterberg Rm |

Mpumalanga Rm |

Tied Rm |

Other Rm |

Energy Rm |

|||||

| External revenue | 15 449 | 8 037 | 4 355 | 34 | 889 | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| Segmental net operating profit/(loss) | 6 668 | (2 419) | 145 | (114) | 1 619 | |||||

| – Continuing operations | 6 668 | (2 419) | 145 | (114) | 1 619 | |||||

| – Discontinued operations | ||||||||||

| External finance income (note 10) | 33 | 3 | 8 | 12 | ||||||

| External finance costs (note 10) | (48) | (171) | (52) | (402) | ||||||

| Income tax (expense)/benefit | (2 020) | 530 | (46) | 782 | 1 | |||||

| – Continuing operations | (2 020) | 530 | (46) | 782 | 1 | |||||

| – Discontinued operations | ||||||||||

| Depreciation and amortisation (note 8) | (1 373) | (611) | (19) | (2) | (291) | |||||

| Impairment charges (note 9) | (1 378) | |||||||||

| Gain on deemed disposal of JV (note 4) | 1 321 | |||||||||

| Gains on disposal of joint operation and transfer of operation (note 8) | 17 | 4 | ||||||||

| Share of income/(loss) of equity-accounted investments (note 11) | 67 | 5 | (5) | |||||||

| – Continuing operations | 67 | 5 | (5) | |||||||

| – Discontinued operations | ||||||||||

| Cash generated by/(utilised in) operations | 8 223 | (879) | 241 | (1 717) | 693 | |||||

| Capital spend (note 13) | (2 326) | (717) | (1) | (16) | (1) | |||||

| At 31 December 2020 (Reviewed) | ||||||||||

| Segmental assets and liabilities | ||||||||||

| Deferred tax1 | 112 | (158) | 589 | 146 | ||||||

| Equity-accounted investments (note 15) | 1 412 | 2 053 | 98 | |||||||

| External assets | 30 155 | 6 160 | 1 138 | 2 468 | 8 825 | |||||

| Assets | 30 155 | 7 684 | 980 | 5 110 | 9 069 | |||||

| Non-current assets held-for-sale (note 17) | 2 008 | |||||||||

| Total assets | 30 155 | 9 692 | 980 | 5 110 | 9 069 | |||||

| External liabilities | 2 129 | 1 288 | 926 | 1 308 | 5 715 | |||||

| Deferred tax1 | 6 934 | 229 | 189 | 937 | ||||||

| Liabilities | 9 063 | 1 517 | 926 | 1 497 | 6 652 | |||||

| Non-current liabilities held-for-sale (note 17) | 1 138 | |||||||||

| Total liabilities | 9 063 | 2 655 | 926 | 1 497 | 6 652 | |||||

| 1 | Offset per legal entity and tax authority. |

| Ferrous | Other | ||||||||||||

| For the year ended 31 December 2020 (Reviewed) | Alloys Rm |

Other ferrous Rm |

TiO2 Rm |

Base metals Rm |

Other Rm | Total Rm |

|||||||

| External revenue | 147 | 13 | 28 924 | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Segmental net operating profit/(loss) | 4 | 93 | (1 703) | 4 293 | |||||||||

| – Continuing operations | 4 | 93 | (1 703) | 4 293 | |||||||||

| – Discontinued operations | |||||||||||||

| External finance income (note 10) | 159 | 215 | |||||||||||

| External finance costs (note 10) | (1) | (373) | (1 047) | ||||||||||

| Income tax (expense)/benefit | 7 | 27 | (719) | ||||||||||

| – Continuing operations | 7 | 27 | (719) | ||||||||||

| – Discontinued operations | |||||||||||||

| Depreciation and amortisation (note 8) | (6) | (134) | (2 436) | ||||||||||

| Impairment charges (note 9) | (504) | (1 882) | |||||||||||

| Gain on deemed disposal of JV (note 4) | 1 321 | ||||||||||||

| Gains on disposal of joint operation and transfer of operation (note 8) | 21 | ||||||||||||

| Share of income/(loss) of equity-accounted investments (note 11) | 6 125 | 207 | 122 | (110) | 6 411 | ||||||||

| – Continuing operations | 6 125 | 207 | 122 | (110) | 6 411 | ||||||||

| – Discontinued operations | |||||||||||||

| Cash generated by/(utilised in) operations | (38) | (4) | 1 251 | 7 770 | |||||||||

| Capital spend (note 13) | (2) | (112) | (3 175) | ||||||||||

| At 31 December 2020 (Reviewed) | |||||||||||||

| Segmental assets and liabilities | |||||||||||||

| Deferred tax1 | 17 | 1 | 369 | 1 076 | |||||||||

| Equity-accounted investments (note 15) | 12 820 | 2 628 | 995 | 20 006 | |||||||||

| External assets | 309 | 26 | 4 694 | 53 775 | |||||||||

| Assets | 326 | 12 847 | 2 628 | 995 | 5 063 | 74 857 | |||||||

| Non-current assets held-for-sale (note 17) | 1 741 | 3 749 | |||||||||||

| Total assets | 326 | 12 847 | 4 369 | 995 | 5 063 | 78 606 | |||||||

| External liabilities | 29 | 3 | 9 713 | 21 111 | |||||||||

| Deferred tax1 | (53) | 8 236 | |||||||||||

| Liabilities | 29 | 3 | 9 660 | 29 347 | |||||||||

| Non-current liabilities held-for-sale (note 17) | 1 138 | ||||||||||||

| Total liabilities | 29 | 3 | 9 660 | 30 485 | |||||||||

| 1 | Offset per legal entity and tax authority. |

| Coal | ||||||||||

| Commercial | ||||||||||

| For the year ended 31 December 2019 (Audited ) (Re-presented)1 | Waterberg Rm |

Mpumalanga Rm |

Tied Rm |

Other Rm |

Energy Rm |

|||||

| External revenue | 14 012 | 7 240 | 4 038 | 292 | ||||||

| Segmental net operating profit/(loss)2 | 5 752 | (318) | 136 | (558) | (58) | |||||

| – Continuing operations | 5 752 | (318) | 136 | (558) | (58) | |||||

| – Discontinued operations | ||||||||||

| External finance income (note 10) | 57 | 21 | 30 | |||||||

| External finance costs (note 10) | (54) | (165) | (27) | |||||||

| Income tax (expense)/benefit | (1 627) | 120 | (47) | 627 | ||||||

| – Continuing operations | (1 627) | 120 | (47) | 627 | ||||||

| – Discontinued operations | ||||||||||

| Depreciation and amortisation (note 8) | (1 383) | (382) | (23) | (3) | ||||||

| Impairment charges (note 9) | 23 | |||||||||

| Loss on loss of control of subsidiary | (35) | |||||||||

| Gain on disposal of operation | 76 | |||||||||

| Share of income/(loss) of equity-accounted investments (note 11) | 127 | 1 | 18 | |||||||

| – Continuing operations | 127 | 1 | 18 | |||||||

| – Discontinued operations | ||||||||||

| Cash generated by/(utilised in) operations | 6 062 | (253) | 201 | (1 042) | ||||||

| Capital spend (note 13) | (2 951) | (2 776) | (90) | |||||||

| At 31 December 2019 (Audited) (Re-presented)1 | ||||||||||

| Segmental assets and liabilities | ||||||||||

| Deferred tax3 | (107) | 340 | ||||||||

| Equity-accounted investments (note 15) | 1 335 | 2 067 | 350 | |||||||

| Loans to associates | 133 | |||||||||

| External assets | 28 832 | 10 499 | 1 210 | 3 951 | ||||||

| Assets | 28 832 | 11 967 | 1 103 | 6 358 | 350 | |||||

| Non-current assets held-for-sale (note 17) | ||||||||||

| Total assets | 28 832 | 11 967 | 1 103 | 6 358 | 350 | |||||

| External liabilities | 1 951 | 2 336 | 938 | 2 684 | ||||||

| Deferred tax3 | 6 411 | 715 | 68 | |||||||

| Liabilities | 8 362 | 3 051 | 938 | 2 752 | ||||||

| Non-current liabilities held-for-sale (note 17) | 1 410 | |||||||||

| Total liabilities | 8 362 | 4 461 | 938 | 2 752 | ||||||

| 1 | Refer note 2.3. |

| 2 | Segmental net operating profit/(loss) has been re-presented to reflect the change in the allocation of corporate costs. |

| 3 | Offset per legal entity and tax authority. |

| Ferrous | Other | ||||||||||||

| For the year ended 31 December 2019 (Audited) (Re-presented)1 | Alloys Rm |

Other ferrous Rm |

TiO2 Rm |

Base metals Rm |

Other Rm |

Total Rm |

|||||||

| External revenue | 130 | 14 | 25 726 | ||||||||||

| Segmental net operating profit/(loss)2 | 6 | (1) | 2 400 | (960) | 6 399 | ||||||||

| – Continuing operations | 6 | (1) | 270 | (960) | 4 269 | ||||||||

| – Discontinued operations | 2 130 | 2 130 | |||||||||||

| External finance income (note 10) | 210 | 318 | |||||||||||

| External finance costs (note 10) | (1) | (108) | (355) | ||||||||||

| Income tax (expense)/benefit | 3 | (65) | (44) | (1 033) | |||||||||

| – Continuing operations | 3 | (44) | (968) | ||||||||||

| – Discontinued operations | (65) | (65) | |||||||||||

| Depreciation and amortisation (note 8) | (5) | (116) | (1 912) | ||||||||||

| Impairment charges (note 9) | (58) | (35) | |||||||||||

| Loss on loss of control of subsidiary | (35) | ||||||||||||

| Gain on disposal of operation | 76 | ||||||||||||

| Share of income/(loss) of equity-accounted investments (note 11) | 4 413 | 234 | 52 | (152) | 4 693 | ||||||||

| – Continuing operations | 4 413 | 234 | 52 | (152) | 4 693 | ||||||||

| – Discontinued operations | |||||||||||||

| Cash generated by/(utilised in) operations | 1 | 304 | 5 273 | ||||||||||

| Capital spend (note 13) | (259) | (6 076) | |||||||||||

| At 31 December 2019 (Audited) (Re-presented)1 | |||||||||||||

| Segmental assets and liabilities | |||||||||||||

| Deferred tax3 | 11 | 223 | 467 | ||||||||||

| Equity-accounted investments (note 15) | 9 835 | 2 472 | 872 | 571 | 17 502 | ||||||||

| Loans to associates | 133 | ||||||||||||

| External assets | 279 | 25 | 65 | 4 136 | 48 997 | ||||||||

| Assets | 290 | 9 860 | 2 537 | 872 | 4 930 | 67 099 | |||||||

| Non-current assets held-for-sale (note 17) | 1 741 | 1 741 | |||||||||||

| Total assets | 290 | 9 860 | 4 278 | 872 | 4 930 | 68 840 | |||||||

| External liabilities | 30 | 6 | 9 460 | 17 405 | |||||||||

| Deferred tax3 | (56) | 7 138 | |||||||||||

| Liabilities | 30 | 6 | 9 404 | 24 543 | |||||||||

| Non-current liabilities held-for-sale (note 17) | 1 410 | ||||||||||||

| Total liabilities | 30 | 6 | 9 404 | 25 953 | |||||||||

| 1 | Refer note 2.3. |

| 2 | Segmental net operating profit/(loss) has been re-presented to reflect the change in the allocation of corporate costs. |

| 3 | Offset per legal entity and tax authority. |

6. DISCONTINUED OPERATIONS

The discontinued operation relates to Tronox Holdings plc, which represents a major geographical area of operation as well as the majority of the TiO2 reportable segment.

Financial information relating to the discontinued operation is set out below:

| For the year ended 31 December | ||||

| 2020 Reviewed Rm |

(Re-presented)1 2019 Audited Rm |

|||

| Financial performance | ||||

| Losses on financial instruments revaluations recycled to profit or loss | (1) | |||

| Net gains on translation differences recycled to profit or loss on partial disposal of investment in foreign associate | 832 | |||

| Indemnification asset movement | 65 | |||

| Operating profit | 896 | |||

| Gain on partial disposal of associate | 1 234 | |||

| Net operating profit | 2 130 | |||

| Dividend income received from non-current assets held-for-sale | 69 | 47 | ||

| Profit before tax | 69 | 2 177 | ||

| Income tax expense | (65) | |||

| Profit for the year from discontinued operations | 69 | 2 112 | ||

| Other comprehensive loss, net of tax | ||||

| Items that have subsequently been reclassified to profit or loss: | (831) | |||

| – Recycling of share of OCI of equity-accounted investments | (831) | |||

| Total comprehensive income for the year | 69 | 1 281 | ||

| Cash flow information | ||||

| Cash flow attributable to investing activities | ||||

| – Dividend income received from non-current assets held-for-sale | 69 | 47 | ||

| – Proceeds from partial disposal of associate classified as non-current assets held-for-sale | 2 889 | |||

| Cash flow attributable to discontinued operations | 69 | 2 936 | ||

| 1 | Refer note 2.3. |

7. REVENUE

Revenue is derived from contracts with customers. Revenue has been disaggregated based on timing of revenue recognition, major type of goods and services, major geographic area and major customer industries.

| Coal | Ferrous | Other | ||||||||||

| Commercial | ||||||||||||

| For the year ended 31 December 2020 (Reviewed) | Water- berg Rm |

Mpuma- langa Rm |

Tied Rm |

Other Rm |

Energy Rm |

Alloys Rm |

Other Rm |

Total Rm |

||||

| Segmental revenue reconciliation | ||||||||||||

| Segmental revenue1 | 15 449 | 8 037 | 4 355 | 34 | 889 | 147 | 13 | 28 924 | ||||

| Export sales allocated to selling entity | (2 002) | (7 357) | 9 359 | |||||||||

| Total revenue | 13 447 | 680 | 4 355 | 9 393 | 889 | 147 | 13 | 28 924 | ||||

| By timing and major type of goods and services | ||||||||||||

| Sale of goods at a point in time | 13 447 | 680 | 3 744 | 9 293 | 889 | 139 | 12 | 28 204 | ||||

| Coal | 13 447 | 680 | 3 744 | 9 293 | 27 164 | |||||||

| Ferrosilicon | 139 | 139 | ||||||||||

| Renewable energy | 889 | 889 | ||||||||||

| Biological goods | 12 | 12 | ||||||||||

| Rendering of services over time | 611 | 100 | 8 | 1 | 720 | |||||||

| Stock yard management services | 154 | 154 | ||||||||||

| Project engineering services | 457 | 457 | ||||||||||

| Other mine management services | 34 | 34 | ||||||||||

| Transportation services | 66 | 2 | 68 | |||||||||

| Other services | 6 | 1 | 7 | |||||||||

| Total revenue | 13 447 | 680 | 4 355 | 9 393 | 889 | 147 | 13 | 28 924 | ||||

| By major geographic area of customer2 | ||||||||||||

| Domestic | 13 447 | 680 | 4 355 | 34 | 889 | 147 | 8 | 19 560 | ||||

| Export | 9 359 | 5 | 9 364 | |||||||||

| Europe | 3 904 | 3 | 3 907 | |||||||||

| Asia | 4 539 | 2 | 4 541 | |||||||||

| Other | 916 | 916 | ||||||||||

| Total revenue | 13 447 | 680 | 4 355 | 9 393 | 889 | 147 | 13 | 28 924 | ||||

| By major customer industries | ||||||||||||

| Public utilities | 11 508 | 4 355 | 260 | 889 | 17 012 | |||||||

| Merchants | 174 | 345 | 8 525 | 2 | 9 046 | |||||||

| Steel | 1 014 | 79 | 77 | 1 170 | ||||||||

| Mining | 56 | 103 | 126 | 119 | 404 | |||||||

| Manufacturing | 275 | 26 | 301 | |||||||||

| Food and beverage | 250 | 8 | 258 | |||||||||

| Chemicals | 145 | 145 | ||||||||||

| Cement | 132 | 132 | ||||||||||

| Other | 38 | 8 | 405 | 5 | 456 | |||||||

| Total revenue | 13 447 | 680 | 4 355 | 9 393 | 889 | 147 | 13 | 28 924 | ||||

| 1 | Coal segmental revenue is based on the origin of coal production. |

| 2 | Determined based on the customer supplied by Exxaro. |

| Coal | Ferrous | Other | ||||||||||

| Commercial | ||||||||||||

| For the year ended 31 December 2019 (Audited) | Water- berg Rm |

Mpuma- langa Rm |

Tied Rm |

Other Rm |

Alloys Rm |

Other Rm |

Total Rm |

|||||

| Segmental revenue reconciliation | ||||||||||||

| Segmental revenue1 | 14 012 | 7 240 | 4 038 | 292 | 130 | 14 | 25 726 | |||||

| Export sales allocated to selling entity | (1 494) | (5 468) | 6 962 | |||||||||

| Total revenue | 12 518 | 1 772 | 4 038 | 7 254 | 130 | 14 | 25 726 | |||||

| By timing and major type of goods and services | ||||||||||||

| Sale of goods at a point in time | 12 518 | 1 721 | 3 414 | 6 870 | 122 | 12 | 24 657 | |||||

| Coal | 12 518 | 1 721 | 3 414 | 6 870 | 24 523 | |||||||

| Ferrosilicon | 122 | 122 | ||||||||||

| Biological goods | 12 | 12 | ||||||||||

| Rendering of services over time | 51 | 624 | 384 | 8 | 2 | 1 069 | ||||||

| Stock yard management services | 130 | 130 | ||||||||||

| Project engineering services | 494 | 494 | ||||||||||

| Other mine management services | 292 | 292 | ||||||||||

| Transportation services | 51 | 92 | 2 | 145 | ||||||||

| Other services | 6 | 2 | 8 | |||||||||

| Total revenue | 12 518 | 1 772 | 4 038 | 7 254 | 130 | 14 | 25 726 | |||||

| By major geographic area of customer2 | ||||||||||||

| Domestic | 12 518 | 1 772 | 4 038 | 292 | 130 | 13 | 18 763 | |||||

| Export | 6 962 | 1 | 6 963 | |||||||||

| Europe | 3 617 | 1 | 3 618 | |||||||||

| Asia | 3 159 | 3 159 | ||||||||||

| Other | 186 | 186 | ||||||||||

| Total revenue | 12 518 | 1 772 | 4 038 | 7 254 | 130 | 14 | 25 726 | |||||

| By major customer industries | ||||||||||||

| Public utilities | 10 211 | 1 009 | 4 038 | 467 | 15 725 | |||||||

| Merchants | 179 | 326 | 6 475 | 6 980 | ||||||||

| Steel | 1 378 | 68 | 43 | 1 489 | ||||||||

| Mining | 81 | 133 | 266 | 103 | 583 | |||||||

| Manufacturing | 279 | 24 | 303 | |||||||||

| Cement | 148 | 148 | ||||||||||

| Food and beverage | 200 | 1 | 201 | |||||||||

| Chemicals | 167 | 167 | ||||||||||

| Other | 42 | 69 | 3 | 3 | 13 | 130 | ||||||

| Total revenue | 12 518 | 1 772 | 4 038 | 7 254 | 130 | 14 | 25 726 | |||||

| 1 | Coal segmental revenue is based on the origin of coal production. |

| 2 | Determined based on the customer supplied by Exxaro. |

8. SIGNIFICANT ITEMS INCLUDED IN OPERATING EXPENSES

| For the year ended 31 December | ||||

| 2020 Reviewed Rm |

2019 Audited Rm |

|||

| The following (expense)/income items are included, among others, in operating expenses: | ||||

| Raw materials and consumables | (3 744) | (3 760) | ||

| Staff costs1 | (5 103) | (5 248) | ||

| Royalties | (575) | (459) | ||

| Contract mining | (2 409) | (2 308) | ||

| Repairs and maintenance | (2 421) | (2 251) | ||

| Railage and transport | (3 101) | (2 353) | ||

| Movement in provisions (note 20) | 1 100 | (127) | ||

| Movement in indemnification asset | (798) | 139 | ||

| Depreciation and amortisation | (2 436) | (1 912) | ||

| – Depreciation of property, plant and equipment | (2 237) | (1 849) | ||

| – Depreciation of right-of-use assets | (71) | (59) | ||

| – Amortisation of intangible assets | (128) | (4) | ||

| Gain on deemed disposal of JV2 | 1 321 | |||

| Losses on share of cash flow hedge reserve recycled to profit or loss on deemed disposal of JV2 | (59) | |||

| Fair value adjustments on contingent consideration3 | (3) | 296 | ||

| Hedge ineffectiveness on cash flow hedges (note 23.2) | (57) | |||

| Legal and professional fees | (653) | (742) | ||

| Net gains on disposal of property, plant and equipment | (92) | |||

| Gain on disposal of joint operation4 | 17 | |||

| Gain on transfer of operation5 | 4 | |||

| Loss on disposal of operation | 76 | |||

| Loss on loss of control of subsidiary | (35) | |||

| Loss on dilution of investment in associates | (20) | (42) | ||

| Gain on disposal of associate | 270 | |||

| ECLs6 | 144 | (165) | ||

| Write down of inventory to net realisable value | (9) | (11) | ||

| Insurance recoveries for | 32 | 148 | ||

| – Business interruption | 14 | 99 | ||

| – Property, plant and equipment | 18 | 49 | ||

| 1 | 2019 includes an amount of R459 million relating to TVPs. |

| 2 | Relates to the step-up acquisition of Cennergi (refer note 4). |

| 3 | 2020: relates to the Cennergi acquisition; 2019: relates to the ECC acquisition. |

| 4 | Relates to EMJV. |

| 5 | Relates to Arnot. |

| 6 | 2020: relates mainly to the reversal of ECLs as payments were received on non-performing other receivables. 2019: relates mainly to non-performing other receivables and the loan to Tumelo. |

9. IMPAIRMENT CHARGES

| For the year ended 31 December | ||||

| 2020 Reviewed Rm |

2019 Audited Rm |

|||

| ECC operation | ||||

| Impairment charges | (1 378) | |||

| – Property, plant and equipment | (1 359) | |||

| – Right-of-use assets | (19) | |||

| Investments in associates | ||||

| Impairment charges | (504) | (58) | ||

| – Insect Technology | (458) | |||

| – Curapipe | (46) | |||

| – GAM | (58) | |||

| Reductants operation | ||||

| Impairment reversal | 23 | |||

| – Property, plant and equipment | 23 | |||

| Net impairment charges | (1 882) | (35) | ||

| Tax effect1 | 236 | |||

| Net effect on attributable earnings | (1 646) | (35) | ||

| 1 | Tax effect relates to the ECC operation. |

ECC operation

On 31 December 2020, the ECC operation, met all the criteria in terms of IFRS 5 Non-current Assets Held for Sale and Discontinued Operations (IFRS 5) to be classified as a non-current asset held-for-sale (refer note 17). An impairment assessment in terms of IAS 36 Impairment of Non-current Assets (IAS 36) was required to be performed. The recoverable amount was determined to be its fair value less costs of disposal (which represents the discounted value of the offer price negotiated with the proposed buyer to the sales transaction).

Insect Technology

During 2020, Exxaro's investment in Insect Technology was no longer considered to be a strategic fit for Exxaro. Consequently Exxaro will not participate in any further fund raising.

Insect Technology was unable to raise funding for pre-commissioning, research and development as well as operational expenses. The delays in the fund raising had an impact on working capital requirements and the company found itself in severe financial distress. Due to the uncertainty of whether Insect Technology will continue as a going concern, a decision was taken to impair the investment.

On 31 December 2020, the equity interest in Insect Technology was impaired to nil.

Curapipe

The investment in Curapipe was identified not to be a strategic fit for Exxaro and as a result, Exxaro embarked on a divestment process during 2020 for the total equity interest in Curapipe. On 30 June 2020, the investment in Curapipe was impaired to US$1. Subsequently, the investment was sold on 9 November 2020.

10. NET FINANCING COSTS

| For the year ended 31 December |

|||||||

| 2020 Reviewed Rm |

2019 Audited Rm |

||||||

| Finance income | 215 | 318 | |||||

|---|---|---|---|---|---|---|---|

| Interest income | 209 | 292 | |||||

| Reimbursement of interest income on environmental rehabilitation funds | (5) | ||||||

| Finance lease interest income | 8 | 9 | |||||

| Commitment fee income | 3 | 6 | |||||

| Interest income from loan to joint venture | 11 | ||||||

| Finance costs | (1 047) | (355) | |||||

| Interest expense | (984) | (506) | |||||

| Net fair value loss on interest rate swaps designated as cash flow hedges: transfer from OCI | (107) | ||||||

| – Realised fair value loss | (153) | ||||||

| – Unrealised fair value gain | 46 | ||||||

| Unwinding of discount rate on rehabilitation costs | (305) | (414) | |||||

| Recovery of unwinding of discount rate on rehabilitation costs | 38 | 167 | |||||

| Interest expense on lease liabilities | (54) | (36) | |||||

| Amortisation of transaction costs | (9) | (14) | |||||

| Borrowing costs capitalised1 | 374 | 448 | |||||

| Total net financing costs | (832) | (37) | |||||

| 1 Borrowing costs capitalisation rate: | 7.79% | 9.98% | |||||

11. SHARE OF INCOME OF EQUITY-ACCOUNTED INVESTMENTS

| For the year ended 31 December |

|||||

| 2020 Reviewed Rm |

(Re-presented)1 2019 Audited Rm |

||||

| Associates | 6 331 | 4 520 | |||

|---|---|---|---|---|---|

| SIOC | 6 125 | 4 413 | |||

| Tronox SA | 207 | 234 | |||

| RBCT | 5 | 1 | |||

| Black Mountain1 | 122 | 52 | |||

| Curapipe2 | (1) | (4) | |||

| Insect Technology | (109) | (148) | |||

| LightApp | (18) | (28) | |||

| Joint ventures | 80 | 173 | |||

| Mafube | 67 | 127 | |||

| Cennergi3 | 13 | 46 | |||

| Share of income of equity-accounted investments | 6 411 | 4 693 | |||

| 1 | The investment in Black Mountain was previously presented as a discontinued operation. Refer note 2.3. |

| 2 | The investment in Curapipe was sold on 9 November 2020. |

| 3 | Equity-accounted income up to 31 March 2020. |

12. DIVIDEND DISTRIBUTIONS

A final cash dividend, number 36, for 2020 of 1 243 cents per share, was approved by the board of directors on 16 March 2021. The dividend is payable on 3 May 2021 to shareholders who will be on the register on 30 April 2021. This final dividend, amounting to approximately R3 119 million (to external shareholders), has not been recognised as a liability in these condensed annual financial statements. It will be recognised in shareholders' equity in the year ending 31 December 2021. The final dividend declared will be subject to a dividend withholding tax of 20% for all shareholders who are not exempt from or do not qualify for a reduced rate of dividend withholding tax. The net local dividend payable to shareholders, subject to dividend withholding tax at a rate of 20% amounts to 994.4000 cents per share. Taking into account the proceeds of R5 763 million received from the disposal of Exxaro's shareholding in Tronox Holdings plc, the board of directors has approved to pay a special dividend of 543 cents per share. The special dividend is payable on 3 May 2021 to shareholders who will be on the register on 30 April 2021. This special dividend, amounting to approximately R1 363 million (to external shareholders), has not been recognised as a liability in these condensed annual financial statements. It will be recognised in shareholder's equity in the year ending 31 December 2021. The special dividend declared will be subject to a dividend withholding tax of 20% for all shareholders who are not exempt from or do not qualify for a reduced rate of dividend withholding tax. The net local dividend payable to shareholders, subject to dividend withholding tax at a rate of 20% amounts to 434.40000 cents per share. The number of ordinary shares in issue at the date of this declaration is 358 706 754. Exxaro company's tax reference number is 9218/098/14/4. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

13. CAPITAL SPEND AND CAPITAL COMMITMENTS

| At 31 December | |||||

| 2020 Reviewed Rm |

2019 Audited Rm |

||||

| Capital spend | |||||

| To maintain operations | 2 225 | 2 502 | |||

| To expand operations | 950 | 3 574 | |||

| Total capital spend | 3 175 | 6 076 | |||

| Capital commitments | |||||

| Contracted | 2 339 | 2 225 | |||

| – Contracted for the group (owner-controlled) | 1 990 | 1 985 | |||

| – Share of capital commitments of equity-accounted investments | 349 | 240 | |||

| Authorised, but not contracted | 1 484 | 3 119 | |||

14. INTANGIBLE ASSETS

| At 31 December | |||||

| 2020 Reviewed Rm |

2019 Audited Rm |

||||

| Goodwill | |||||

| Net carrying amount | |||||

| Acquisition of subsidiaries (note 4) | 521 | ||||

| At end of the year | 521 | ||||

| Contracts with customers | |||||

| Gross carrying amount | |||||

| Acquisition of subsidiaries (note 4) | 2 685 | ||||

| At end of the year | 2 685 | ||||

| Accumulated amortisation | |||||

| Charges for the year | (123) | ||||

| At end of the year | (123) | ||||

| Patents and licences | |||||

| Gross carrying amount | |||||

| At beginning of the year | 43 | 38 | |||

| Additions | 2 | 5 | |||

| Reclassification to non-current assets held-for-sale | (7) | ||||

| Exchange differences | 1 | ||||

| At end of the year | 39 | 43 | |||

| Accumulated amortisation | |||||

| At beginning of the year | (27) | (23) | |||

| Charges for the year | (5) | (4) | |||

| Reclassification to non-current assets held-for-sale | 5 | ||||

| At end of the year | (27) | (27) | |||

| Net carrying amount at end of the year | 3 095 | 16 | |||

15. EQUITY-ACCOUNTED INVESTMENTS

| At 31 December | |||||

| 2020 Reviewed Rm |

(Re-presented)1 2019 Audited Rm |

||||

| Associates | 18 594 | 15 928 | |||

|---|---|---|---|---|---|

| SIOC | 12 820 | 9 835 | |||

| Tronox SA | 2 628 | 2 472 | |||

| RBCT | 2 053 | 2 067 | |||

| Black Mountain | 995 | 872 | |||

| Curapipe2 | 37 | ||||

| Insect Technology3 | 534 | ||||

| LightApp | 98 | 111 | |||

| Joint ventures | 1 412 | 1 574 | |||

| Mafube | 1 412 | 1 335 | |||

| Cennergi4 | 239 | ||||

| Total carrying value of equity-accounted investments | 20 006 | 17 502 | |||

|

16. OTHER ASSETS

| At 31 December | |||||

| 2020 Reviewed Rm |

2019 Audited Rm |

||||

| Non-current | |||||

| Reimbursements1 | 373 | 1 648 | |||

| Indemnification asset: Total S.A.2 | 1 410 | ||||

| Biological assets | 28 | 24 | |||

| Lease receivables | 53 | 61 | |||

| Deferred costs | 2 | ||||

| Other | 74 | 51 | |||

| Total non-current other assets | 530 | 3 194 | |||

| Current | |||||

| Indemnification asset: Tronox Holdings plc | 65 | ||||

| VAT | 504 | 501 | |||

| Royalties | 127 | 114 | |||

| Prepayments | 144 | 120 | |||

| Current tax receivables | 198 | 265 | |||

| Lease receivables | 6 | 6 | |||

| Other | 41 | 33 | |||

| Total current other assets | 1 020 | 1 104 | |||

| Total other assets | 1 550 | 4 298 | |||

|

17. NON-CURRENT ASSETS AND LIABILITIES HELD-FOR-SALE

ECC operation The ECC operation was identified as non-core to the future objectives of Exxaro. As a result, Exxaro embarked on a divestment process of the total equity interest in ECC. The ECC operation is reported as part of the coal Mpumalanga reportable segment and does not meet the criteria to be classified as a discontinued operation since it does not represent a separate major line of business, nor does it represent a major geographical area of operation. Tronox Holdings plc In September 2017, the directors of Exxaro formally decided to dispose of the investment in Tronox Limited. As part of this decision, Tronox Limited was required to publish an automatic shelf registration statement of securities of well-known seasoned issuers which allowed for the conversion of Exxaro's Class B Tronox Limited ordinary shares to Class A Tronox Limited ordinary shares. From this point, it was concluded that the Tronox Limited investment should be classified as a non-current asset held-for-sale as all the criteria in terms of IFRS 5 were met. As of 30 September 2017, the Tronox Limited investment, totalling 42.66% of Tronox Limited's total outstanding voting shares, was classified as a non-current asset held-for-sale and the application of the equity method ceased. Subsequently, Exxaro sold 22 425 000 Class A Tronox Limited ordinary shares during October 2017. During May 2019, Tronox Holdings plc repurchased The Tronox Holdings plc investment is presented within the total assets of the TiO2 reportable segment and is presented as a discontinued operation (refer note 6). Subsequent to year-end, the remaining 14 729 280 shares were sold on 1 March 2021 (refer note 27). EMJV As part of the ECC acquisition in 2015, Exxaro acquired non-current liabilities held-for-sale relating to the EMJV. The transaction was conditional on a section 43 consent required in terms of the MPRDA for transfer of the legal environmental liabilities and rehabilitation obligations to Scinta Energy Proprietary Limited. On 31 December 2020, all conditions precedent to the transaction were met and the transaction became effective. The major classes of assets and liabilities classified as non-current assets and liabilities held-for-sale areas follows: |

| At 31 December | ||||

| 2020 Reviewed Rm |

(Re-presented)1 2019 Audited Rm |

|||

| Assets | ||||

| Property, plant and equipment | 841 | |||

| Right-of-use assets | 1 | |||

| Intangible assets | 2 | |||

| Investments in associates | 1 741 | 1 741 | ||

| – Tronox Holdings plc | 1 741 | 1 741 | ||

| Non-current financial assets | 655 | |||

| – Environmental rehabilitation funds | 655 | |||

| Inventories | 149 | |||

| Current financial assets | 139 | |||

| – Loans to associate: Tumelo | 139 | |||

| Trade and other receivables | 39 | |||

| – Trade receivables | 29 | |||

| – Other receivables | 10 | |||

| Other current assets | 153 | |||

| Current tax receivable | 21 | |||

| Cash and cash equivalents | 8 | |||

| Non-current assets held-for-sale | 3 749 | 1 741 | ||

| Liabilities | ||||

| Non-current lease liabilities | (13) | |||

| Other non-current payables | (7) | |||

| Non-current provisions | (724) | (1 393) | ||

| Retirement employee obligations | (1) | (17) | ||

| Deferred tax liabilities | (21) | |||

| Trade and other payables | (289) | |||

| – Trade payables | (76) | |||

| – Other payables | (213) | |||

| Current lease liabilities | (8) | |||

| Current provisions | (2) | |||

| Current tax payable | (1) | |||

| Other current liabilities | (72) | |||

| Non-current liabilities held-for-sale | (1 138) | (1 410) | ||

| Net non-current assets held-for-sale | 2 611 | 331 | ||

|

18. INTEREST-BEARING BORROWINGS

| At 31 December | |||||

| 2020 Reviewed Rm |

2019 Audited Rm |

||||

| Non-current1 | 7 448 | 6 991 | |||

|---|---|---|---|---|---|

| Loan facility2 | 1 748 | 5 991 | |||

| Project financing3 | 4 700 | ||||

| Bonds | 1 000 | 1 000 | |||

| Current1 | 6 163 | 50 | |||

| Loan facility2 | 6 050 | 46 | |||

| Project financing3 | 110 | ||||

| Bonds | 3 | 4 | |||

| Total interest-bearing borrowings | 13 611 | 7 041 | |||

| Summary of interest-bearing borrowings by period of redemption: | |||||

| Less than six months | 107 | 54 | |||

| Six to 12 months | 6 056 | (4) | |||

| Between one and two years | 1 379 | 2 744 | |||

| Between two and three years | 1 082 | 3 605 | |||

| Between three and four years | 915 | (1) | |||

| Between four and five years | 349 | 643 | |||

| Over five years | 3 723 | ||||

| Total interest-bearing borrowings | 13 611 | 7 041 | |||

| 1 Reduced by the amortisation of transaction costs of: | |||||

| – Non-current | (2) | (9) | |||

| – Current | (6) | (9) | |||

| 2 Exxaro is in the process of refinancing its loan facility as the current facility is expected to mature in July 2021. | |||||

| 3 Interest-bearing borrowings relating to the Cennergi group. | |||||

| Overdraft | |||||

| Bank overdraft | 17 | 976 | |||

|

The bank overdraft is repayable on demand. Interest is based on current South African money market rates. There were no defaults or breaches in terms of interest-bearing borrowings during the reporting periods, except for a technical non-compliance in relation to the project financing agreements which was rectified before the end of the year as agreed with the financial institutions. Below is a summary of the salient terms and conditions of the facilities: |

| Loan facility | |||||||||

| Year | Bullet term loan | Amortised term loan |

Revolving1 facility |

||||||

| Aggregate nominal amount (Rm) | 2020 | 3 250 | 1 750 | 4 750 | |||||

|---|---|---|---|---|---|---|---|---|---|

| 2019 | 3 250 | 1 750 | 2 750 | ||||||

| Issue date or draw down date | 29 July 2016 | 29 July 2016 | 29 July 2016 | ||||||

| Maturity date | 29 July 2021 | 29 July 2023 | 29 July 2021 | ||||||

| Capital payments | The total outstanding amount is payable on final maturity date | Four consecutive semi-annual instalments commencing on the date occurring 18 months prior to the final maturity date | The total outstanding amount is payable on final maturity date | ||||||

| Duration (months) | 60 | 84 | 60 | ||||||

| Secured or unsecured | Unsecured | Unsecured | Unsecured | ||||||

| Undrawn portion (Rm) | 2020 | nil | nil | 2 000 | |||||

| 2019 | nil | 1 750 | nil | ||||||

| Interest | |||||||||

| Interest payment basis | Floating rate | Floating rate | Floating rate | ||||||

| Interest payment period | Three months | Three months | Monthly | ||||||

| Interest rate | 3-month JIBAR plus a margin of 325 basis points (3.25%) |

3-month JIBAR plus a margin of 360 basis points (3.60%) |

1-month JIBAR plus a margin of 325 basis points (3.25%) |

||||||

| Effective interest rates for the transaction costs | 2020 | 0.17% | N/A | N/A | |||||

| 2019 | 0.17% | N/A | N/A | ||||||

|

| Project financing1 | |||||||||

| Year | Tsitsikamma SPV loan facility |

Amakhala SPV loan facilities: floating rate2 |

Amakhala SPV loan facilities: fixed rate3 |

||||||

| Remaining nominal amount outstanding (Rm) | 2020 | 1 918 | 2 734 | 158 | |||||

|---|---|---|---|---|---|---|---|---|---|

| Debt assumed date | 1 April 2020 | 1 April 2020 | 1 April 2020 | ||||||

| Maturity date | 31 December 2030 | 30 June 2031 | 30 June 2031 | ||||||

| Capital payments | Bi-annual installments ranging incrementally over the term from 0.18% to 10.65% of the nominal amount | Bi-annual installments ranging incrementally over the term from 0.18% to 10.65% of the nominal amount | Bi-annual installments ranging incrementally over the term from 0.18% to 10.65% of the nominal amount | ||||||

| Duration (months) | 129 | 135 | 135 | ||||||

| Secured or unsecured4 | Secured | Secured | Secured | ||||||

| Undrawn portion (Rm) | 2020 | 122 | 273 | ||||||

| Interest5 | |||||||||

| Interest payment basis | Floating rate | Floating rate | Fixed rate | ||||||

| Interest payment period | Bi-annual | Bi-annual | Bi-annual | ||||||

| Interest rate | 3-month JIBAR plus a margin of 264 basis points (2.64%) |

3-month JIBAR plus an all in margin ranging from 359 basis points to 681 basis points (3.59% to 6.81%) |

An all in margin ranging from 371 basis points to 681 basis points (3.71% to 6.81%) plus:(1) 8.00% until June 2021 (2) 9.46% from July 2021 to maturity |

||||||

| Effective interest rates for the transaction costs | 2020 | N/A | N/A | N/A | |||||

|

|||||||||||||||||||||||||||||||||||||

| DMTN Programme (bonds) | |||||||||

| Year | R357 million senior unsecured floating rate note |

R643 million senior unsecured floating rate note |

|||||||

| Aggregate nominal amount (Rm) | 2020 | 357 | 643 | ||||||

|---|---|---|---|---|---|---|---|---|---|

| 2019 | 357 | 643 | |||||||

| Issue date or draw down date | 13 June 2019 | 13 June 2019 | |||||||

| Maturity date | 13 June 2022 | 13 June 2024 | |||||||

| Capital payments | No fixed or determined payments, the total outstanding amount is payable on final maturity date | No fixed or determined payments, the total outstanding amount is payable on final maturity date | |||||||

| Duration (months) | 36 | 60 | |||||||

| Secured or unsecured | Unsecured | Unsecured | |||||||

| Interest | |||||||||

| Interest payment basis | Floating rate | Floating rate | |||||||

| Interest payment period | Three months | Three months | |||||||

| Interest rate | 3-month JIBAR plus a margin of 165 basis points (1.65%) | 3-month JIBAR plus a margin of 189 basis points (1.89%) | |||||||

| Effective interest rates for the transaction costs | 2020 | N/A | N/A | ||||||

| 2019 | N/A | N/A | |||||||

19. LEASE LIABILITIES

| At 31 December | ||||

| 2020 Reviewed Rm |

2019 Audited Rm |

|||

| Non-current | 493 | 461 | ||

|---|---|---|---|---|

| Current | 29 | 27 | ||

| Total lease liabilities | 522 | 488 | ||

| Summary of lease liabilities by period of redemption: | ||||

| Less than six months | 14 | 15 | ||

| Six to 12 months | 15 | 12 | ||

| Between one and two years | 34 | 28 | ||

| Between two and three years | 43 | 34 | ||

| Between three and four years | 43 | 34 | ||

| Between four and five years | 53 | 43 | ||

| Over five years | 320 | 322 | ||

| Total lease liabilities | 522 | 488 | ||

| Analysis of movement in lease liabilities | ||||

| At beginning of the year | 488 | 2 | ||

| Recognised on initial application of IFRS 16 Leases | 66 | |||

| Balance at 1 January | 488 | 68 | ||

| New leases | 24 | 458 | ||

| Lease terminations | (12) | |||

| Acquisition of subsidiaries | 55 | |||

| Reclassification to non-current liabilities held-for sale | (21) | |||

| Lease remeasurement adjustments | 10 | 7 | ||

| Lease modification adjustments | (3) | |||

| Exchange difference on translation | 1 | |||

| Capital repayments | (32) | (33) | ||

| – Lease payments | (86) | (69) | ||

| – Interest charges | 54 | 36 | ||

| At end of the year | 522 | 488 | ||

The lease liabilities relate to the right-of-use assets. Interest is based on incremental borrowing rates ranging between 7.33% and 10.44% (2019: 7.85% and 10.44%).

20. PROVISIONS

| Environmental rehabilitation | ||||||||

| Restoration Rm |

Decommis- sioning Rm |

Residual impact Rm |

Other site closure costs Rm |

Other1 Rm |

Total Rm |

|||

| At 31 December 2020 | ||||||||

| At beginning of the year | 2 432 | 544 | 1 345 | 83 | 4 404 | |||

| Charge to operating expenses (note 8) | (60) | (85) | (986) | 14 | 17 | (1 100) | ||

| – Additional provisions | 316 | 14 | 44 | 16 | 17 | 407 | ||

| – Unused amounts reversed2 | (376) | (99) | (1 030) | (2) | (1 507) | |||

| Unwinding of discount rate on rehabilitation costs (note 10) | 169 | 44 | 92 | 305 | ||||

| Provisions capitalised to property, plant and equipment | (88) | (88) | ||||||

| Utilised during the year | (18) | (3) | (16) | (3) | (40) | |||

| Reclassification to non-current liabilities held-for-sale | (467) | (52) | 576 | (2) | 55 | |||

| Acquisition of subsidiaries | 6 | 29 | 4 | 39 | ||||

| Transfer of operation | (642) | (97) | (705) | (1 444) | ||||

| Total provisions at end of the year | 1 420 | 295 | 323 | 79 | 14 | 2 131 | ||

| – Non-current | 1 284 | 295 | 300 | 60 | 7 | 1 946 | ||

| – Current | 136 | 23 | 19 | 7 | 185 | |||

| At 31 December 2019 | ||||||||

| At beginning of the year | 2 516 | 451 | 975 | 80 | 4 022 | |||

| Charge to operating expenses (note 8) | (244) | 52 | 301 | 18 | 127 | |||

| – Additional provisions | 374 | 56 | 403 | 19 | 852 | |||

| – Unused amounts reversed | (618) | (4) | (102) | (1) | (725) | |||

| Unwinding of discount rate on rehabilitation costs (note 10) | 228 | 47 | 139 | 414 | ||||

| Provisions capitalised to property, plant and equipment | (4) | (4) | ||||||

| Utilised during the year | (58) | (15) | (73) | |||||

| Reclassification to non-current liabilities held-for-sale | (4) | (69) | (73) | |||||

| Loss of control of subsidiary | (6) | (2) | (1) | (9) | ||||

| Total provisions at end of the year | 2 432 | 544 | 1 345 | 83 | 4 404 | |||

| – Non-current | 2 366 | 544 | 1 334 | 61 | 4 305 | |||

| – Current | 66 | 11 | 22 | 99 | ||||

| 1 | Relates to a constructive obligation created with certain BEE minorities within the Cennergi group to receive distributions in proportion to their percentage interest prior to their in substance share options being exercised. |

| 2 | The residual impact includes an adjustment to the EMJV environmental rehabilitation provision, amounting to R818 million. |

21. NET DEBT

| At 31 December | ||||

| 2020 Reviewed Rm |

2019 Audited Rm |

|||

| Net debt is presented by the following items on the statement of financial position: | ||||

| Non-current interest-bearing debt | (7 954) | (7 452) | ||

| Interest-bearing borrowings | (7 448) | (6 991) | ||

| Lease liabilities | (493) | (461) | ||

| Lease liabilities classified as non-current liabilities held-for-sale | (13) | |||

| Current interest-bearing debt | (6 200) | (77) | ||

| Interest-bearing borrowings | (6 163) | (50) | ||

| Lease liabilities | (29) | (27) | ||

| Lease liabilities classified as non-current liabilities held-for-sale | (8) | |||

| Net cash and cash equivalents | 3 187 | 1 719 | ||

| Cash and cash equivalents | 3 196 | 2 695 | ||

| Cash and cash equivalents classified as non-current assets held-for-sale | 8 | |||

| Overdraft | (17) | (976) | ||

| Total net debt | (10 967) | (5 810) | ||

Analysis of movement in net debt:

| Liabilities arising from financing activities | ||||||||||

| Cash and cash equivalents/ (overdraft) Rm |

Non- current interest- bearing debt Rm |

Current interest- bearing debt Rm |

Total Rm |

|||||||

| Net debt at 31 December 2018 (Audited) | 549 | (3 843) | (573) | (3 867) | ||||||

| Cash flows | 1 171 | (3 148) | 553 | (1 424) | ||||||

| Operating activities1 | 3 483 | 3 483 | ||||||||

| Investing activities | 2 974 | 2 974 | ||||||||

| Financing activities1 | (5 286) | (3 148) | 553 | (7 881) | ||||||

| – Interest-bearing borrowings raised | 4 250 | (3 750) | (500) | |||||||

| – Interest-bearing borrowings repaid | (1 622) | 602 | 1 020 | |||||||

| – Lease liabilities paid | (33) | 33 | ||||||||

| – Dividends paid to owners of the parent1 | (5 812) | (5 812) | ||||||||

| – Shares acquired in the market to settle share-based payments | (678) | (678) | ||||||||

| – Dividends paid to BEE Parties | (1 391) | (1 391) | ||||||||

| Non-cash movements | (1) | (461) | (57) | (519) | ||||||

| Amortisation of transaction costs | (14) | (14) | ||||||||

| Preference dividend accrued | 13 | 13 | ||||||||

| Interest accrued | 2 | 2 | ||||||||

| Lease remeasurements | (7) | (7) | ||||||||

| New leases | (524) | (524) | ||||||||

| Lease liabilities cancelled | 12 | 12 | ||||||||

| Transfers between non-current and current liabilities | 57 | (57) | ||||||||

| Translation difference on movement in cash and cash equivalents | (1) | (1) | ||||||||

| Net debt at 31 December 2019 (Audited) | 1 719 | (7 452) | (77) | (5 810) | ||||||

| 1 | Dividends paid to owners of the parent have been re-presented as a financing activity (previously presented as an operating activity). |

| Liabilities arising from financing activities | ||||||||||

| Cash and cash equivalents/ (overdraft) Rm |

Non- current interest- bearing debt Rm |

Current interest- bearing debt Rm |

Total Rm |

|||||||

| Net debt at 31 December 2019 (Audited) | 1 719 | (7 452) | (77) | (5 810) | ||||||

| Cash flows | 1 468 | (1 750) | 120 | (162) | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Operating activities | 5 493 | 5 493 | ||||||||

| Investing activities | (1 556) | (1 556) | ||||||||

| Financing activities | (2 469) | (1 750) | 120 | (4 099) | ||||||

| – Interest-bearing borrowings raised | 1 750 | (1 750) | ||||||||

| – Interest-bearing borrowings repaid | (88) | 88 | ||||||||

| – NCI option exercised | 115 | 115 | ||||||||

| – Distributions to NCI option holders | (1) | (1) | ||||||||

| – Loan from NCI | 69 | 69 | ||||||||

| – Lease liabilities paid | (32) | 32 | ||||||||

| – Dividends paid to owners of the parent | (3 034) | (3 034) | ||||||||

| – Shares acquired in the market to settle share-based payments | (270) | (270) | ||||||||

| – Dividends paid to BEE Parties | (978) | (978) | ||||||||

| Non-cash movements | 1 248 | (6 243) | (4 995) | |||||||

| Amortisation of transaction costs | (9) | (9) | ||||||||

| Interest accrued | 114 | 114 | ||||||||

| Lease remeasurements and modifications | (7) | (7) | ||||||||

| New leases | (24) | (24) | ||||||||

| Acquisition of subsidiaries (note 4) | (4 847) | (222) | (5 069) | |||||||

| – Leases | (48) | (7) | (55) | |||||||

| – Project financing | (4 799) | (215) | (5 014) | |||||||

| Transfers between non-current and current liabilities | 6 126 | (6 126) | ||||||||

| Net debt at 31 December 2020 (Reviewed) | 3 187 | (7 954) | (6 200) | (10 967) | ||||||

22. OTHER LIABILITIES

| At 31 December | |||||||

| 2020 Reviewed Rm |

2019 Audited Rm |

||||||

| Non-current | |||||||

| Termination benefits1 | 144 | ||||||

| Income received in advance | 27 | 23 | |||||

| Total non-current other liabilities | 27 | 167 | |||||

| Current | |||||||

| Termination benefits1 | 205 | 305 | |||||

| Leave pay | 225 | 203 | |||||

| Bonuses | 271 | 241 | |||||

| VAT | 31 | 21 | |||||

| Royalties | 9 | ||||||

| Carbon tax | 5 | ||||||

| Current tax payables | 34 | 50 | |||||

| Other current liabilities | 90 | 97 | |||||

| Total current other liabilities | 861 | 926 | |||||

| Total other liabilities | 888 | 1 093 | |||||

| 1 | During 2019, Exxaro announced the implementation of TVPs. Under this policy, employees that qualified would receive a severance package in exchange for termination of employment. |

23. FINANCIAL INSTRUMENTS

The group holds the following financial instruments:

| At 31 December | |||||||

| 2020 Reviewed Rm |

2019 Audited Rm |

||||||

| Non-current | |||||||

| Financial assets | |||||||

| Financial assets at FVOCI | 222 | 235 | |||||

| Equity: unlisted – Chifeng | 222 | 235 | |||||

| Financial assets at FVPL | 1 247 | 2 039 | |||||

| Debt: unlisted – environmental rehabilitation funds | 1 247 | 2 039 | |||||

| Financial assets at amortised cost | 672 | 400 | |||||

| ESD loans1 | 79 | 124 | |||||

| Other financial assets at amortised cost | 593 | 276 | |||||

| – Environmental rehabilitation funds | 386 | ||||||

| – Deferred pricing receivable2 | 212 | 279 | |||||

| – Impairment allowances | (5) | (3) | |||||

| Financial liabilities | |||||||

| Financial liabilities at amortised cost | (7 541) | (7 112) | |||||

| Interest-bearing borrowings | (7 448) | (6 991) | |||||

| Other payables | (24) | (121) | |||||

| Loan from NCI3 | (69) | ||||||

| Derivative financial liabilities designated as hedging instruments | (713) | ||||||

| Hedging derivatives – interest rate swaps4 | (713) | ||||||

| 1 | Interest-free loans advanced to successful applicants in terms of the Exxaro ESD programme. |

| 2 | Relates to a deferred pricing adjustment which arose during 2017. The amount receivable will be settled over seven years (ending 2024) and bears interest at Prime Rate less 2% |

| 3 | Loan payable to a BEE minority shareholder of Tsitsikamma SPV. The loan bears interest at a fixed rate of 16.3%, is unsecured and has no fixed terms of repayment, but is subject to cash being available and covenants approvals from the project financiers. |

| 4 | Refer note 23.2. |

| At 31 December | |||||||

| 2020 Reviewed Rm |

2019 Audited Rm |

||||||

| Current | |||||||

| Financial assets | |||||||

| Financial assets at amortised cost | 6 192 | 6 208 | |||||

| Loans to associates and joint ventures | 133 | ||||||

| Associates | 133 | ||||||

| – Tumelo1 | 182 | ||||||

| – Impairment allowances | (49) | ||||||

| ESD loans2 | 105 | 82 | |||||

| – Gross | 106 | 83 | |||||

| – Impairment allowances | (1) | (1) | |||||

| Other financial assets at amortised cost | 64 | 57 | |||||

| – Deferred pricing receivable3 | 64 | 57 | |||||

| – Deferred consideration receivable4 | 1 | 1 | |||||

| – Employee receivables | 4 | 5 | |||||

| – Impairment allowances | (5) | (6) | |||||

| Trade and other receivables | 2 827 | 3 241 | |||||

| Trade receivables | 2 698 | 2 928 | |||||

| – Gross | 2 793 | 3 023 | |||||

| – Impairment allowances | (95) | (95) | |||||

| Other receivables | 129 | 313 | |||||

| – Gross | 153 | 464 | |||||

| – Impairment allowances | (24) | (151) | |||||

| Cash and cash equivalents | 3 196 | 2 695 | |||||

| Financial liabilities | |||||||

| Financial liabilities at amortised cost | (9 120) | (3 936) | |||||

| Interest-bearing borrowings | (6 163) | (50) | |||||

| Deferred consideration payable5 | (307) | ||||||

| Trade and other payables | (2 940) | (2 603) | |||||

| – Trade payables | (1 371) | (1 164) | |||||

| – Other payables | (1 569) | (1 439) | |||||

| Overdraft | (17) | (976) | |||||

| Financial liabilities at FVPL | (49) | (191) | |||||

| Derivative financial liabilities | (49) | ||||||

| Contingent consideration6 | (191) | ||||||

| 1 | Loan granted to Tumelo. The loan is interest free, unsecured and repayable on demand, unless otherwise agreed by the parties. |

| 2 | Interest-free loans advanced to successful applicants in terms of the Exxaro ESD programme. |

| 3 | Relates to a deferred pricing adjustment which arose during 2017. The amount receivable will be settled over seven years (ending 2024) and bears interest at Prime Rate less 2%. |

| 4 | Relates to deferred consideration receivable which arose on the disposal of mineral properties. |

| 5 | Relates to deferred consideration payable in relation to the acquisition of the investment in Insect Technology. |

| 6 | Relates to the ECC contingent consideration which was fully settled in January 2020. |

The group has granted the following loan commitments:

| At 31 December | ||||

| 2020 Reviewed Rm |

2019 Audited Rm |

|||

| Total loan commitment | 981 | 1 206 | ||

|---|---|---|---|---|

| Mafube1 | 250 | 500 | ||

| Insect Technology2 | 731 | 706 | ||

| Undrawn loan commitment | 981 | 1 206 | ||

| Mafube | 250 | 500 | ||

| Insect Technology | 731 | 706 | ||

| 1 | Revolving credit facility available for five years, ending 2023. |

| 2 | A US$50 million term loan facility available from 2020 to 2025 subject to certain conditions being met. On 31 January 2021 the term loan facility lapsed. |

| 23.1 | Fair value hierarchy | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

The table below analyses recurring fair value measurements for financial assets and financial liabilities. These fair value measurements are categorised into different levels in the fair value hierarchy based on the inputs to the valuation techniques used. The different levels are defined as follows:

Reconciliation of financial assets and financial liabilities within Level 3 of the hierarchy:

Transfers The group recognises transfers between levels of the fair value hierarchy at the end of the reporting period during which the transfer has occurred. There were no transfers between Level 1 and Level 2 nor between Level 2 and Level 3 of the fair value hierarchy. Valuation process applied The fair value computations of the investments are performed by the group's corporate finance department, reporting to the finance director, on a six-monthly basis. The valuation reports are discussed with the chief operating decision maker and the audit committee in accordance with the group's reporting governance. Current derivative financial instruments Level 2 fair values for simple over-the-counter derivative financial instruments are based on market quotes. These quotes are assessed for reasonability by discounting estimated future cash flows using the market rate for similar instruments at measurement date. Environmental rehabilitation funds Level 2 fair values for debt instruments held in the environmental rehabilitation funds are based on quotes provided by the financial institutions at which the funds are invested at measurement date. These financial institutions invest in instruments which are listed. Interest rate swaps Level 2 fair values for interest rate swaps are based on valuations provided by the financial institutions with whom the swaps have been entered into and take into account credit risk. The valuations are assessed for reasonability by discounting the estimated future cash flows based on observable ZAR swap curves. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 23.2 | Hedge accounting: Cash flow hedges | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 23.2.1 | Accounting policy: Hedge accounting | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||