| 2023 (Rm) |

2022 (Rm) |

|||

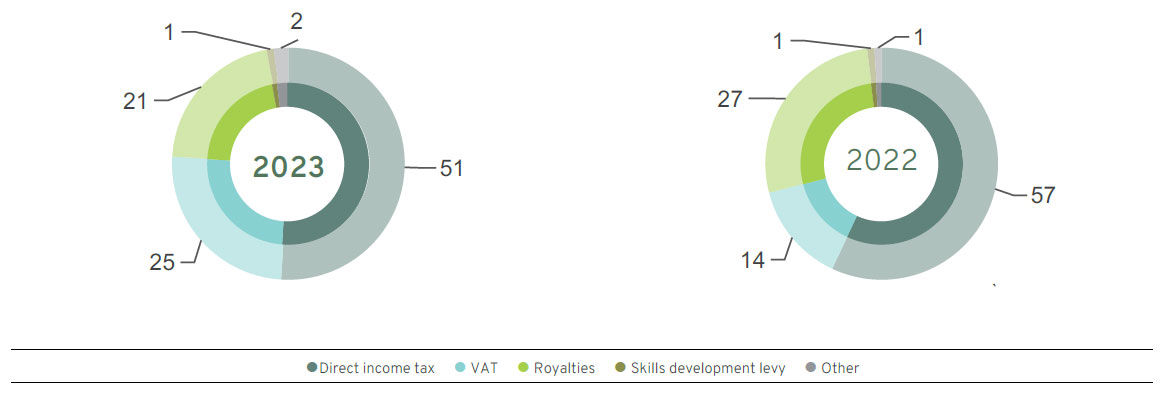

| Payments to government (taxation contribution) | 5 040 | 7 250 | ||

|---|---|---|---|---|

| Direct taxes per country | 2 573 | 4 110 | ||

| South Africa | 2 506 | 4 086 | ||

| Switzerland | 67 | 24 | ||

| Indirect taxes | 1 278 | 1 036 | ||

| VAT* | 1 248 | 1 025 | ||

| Levied on purchases of goods and services | (3 457) | (3 276) | ||

| Charged on turnover | 4 705 | 4 301 | ||

| Dividend withholding tax – local | 1 | 1 | ||

| Dividend withholding tax – Switzerland | 29 | 10 | ||

| Levies paid to government | 1 189 | 2 104 | ||

| Rates and taxes | 21 | 25 | ||

| Mineral and petroleum resources royalty | 1 076 | 1 988 | ||

| Compensation Fund | 17 | 17 | ||

| Unemployment Insurance Fund | 15 | 15 | ||

| Carbon tax | 3 | 3 | ||

| Skills development levy | 57 | 56 | ||

* In 2023, there was a change in the sales mix, resulting in a reduction in exports sales and an increase in local sales. Accordingly, the change in the VAT contribution is attributable to the increased taxable supplies to local vendors, whereas export sales are zero-rated.

| 2023 (Rm) |

2022 (Rm) |

|

| Additional amounts collected by the group on behalf of government | 1 667 | 1 622 |

|---|---|---|

| Unemployment Insurance Fund | 15 | 15 |

| Pay As You Earn tax deducted from remuneration paid | 1 652 | 1 607 |

Total tax contribution paid (%)

The difference in the standard rate of 27% is explained below.

| For the year ended 31 December | 2023 (%) |

2022 (%) |

| Tax as a percentage of profit before tax | 18.0 | 19.2 |

|---|---|---|

| Tax effect of: | ||

| – Net capital losses1 | (0.1) | 0.0 |

| – Impairment charges | 0.0 | (0.1) |

| – Other deductible/(non-deductible) tax adjustments2 | 0.9 | (0.1) |

| – Exempt income3 | 0.1 | 0.1 |

| – Reduction in tax rate | 0.0 | 1.4 |

| – Post-tax equity-accounted income4 | 10.5 | 8.1 |

| – Remeasurements of foreign tax rate differences | 0.2 | 0.3 |

| – Prior year tax adjustments5 | (1.1) | 0.2 |

| – Deferred tax assets not recognised6 | (0.8) | (0.3) |

| – Expected credit losses on financial assets at amortised cost | (0.1) | (0.1) |

| – Dividend withholding tax7 | (0.2) | (0.1) |

| – Imputed income from controlled foreign companies and investments8 | (0.4) | (0.6) |

| Standard tax rate | 27.0 | 28.0 |

| Effective tax rate, excluding income from equity-accounted investments | 29.5 | 27.1 |

| 1 Relates to the disposal of non-allowance assets | ||

| 2 Other deductible/(non-deductible) for tax purposes: | 0.9 | (0.1) |

| – Consulting, legal and other professional fees | (0.2) | (0.1) |

| – Enterprise supplier development grants | 0.0 | (0.1) |

| – Share-based payments | 0.6 | 0.2 |

| – Distribution to beneficiaries of Exxaro ESOP Trust | (0.2) | (0.4) |

| – Other9 | 0.7 | 0.3 |

| 3 | Mainly relates to dividends received by Exxaro ESOP Trust and the NPC (tax-exempt institutions).. |

| 4 | Equity-accounted investment income increased by 7.9%, however, net income before tax decreased by 19.5% from the prior year. The effect that equity-accounted investment income has on the effective tax rate is therefore greater. |

| 5 | Differences between the prior year accrual for normal tax and final tax returns submitted to SARS and a provision of R113 million raised for ongoing disputes with SARS relating to Exxaro Coal and Exxaro Coal Mpumalanga. |

| 6 | Increased losses in Coastal Coal Proprietary Limited, Ferroland Grondtrust Proprietary Limited and Cennergi Holdings Proprietary Limited on which no deferred tax assets are recognised. |

| 7 | Dividend withholding tax paid in Switzerland by EITAG on dividends declared to Rocsi. The dividend paid in February 2023 was based on EITAG's 2022 results, which were 57% higher than the current year. The significant increase is due to double the amount of dividends being paid in the current year compared to the prior year. |

| 8 | Relates to reduced imputed income from EITAG in terms of section 9D of the Income Tax Act due to a reduction in international coal prices and volumes. |

| 9 | This includes foreign tax credits. |

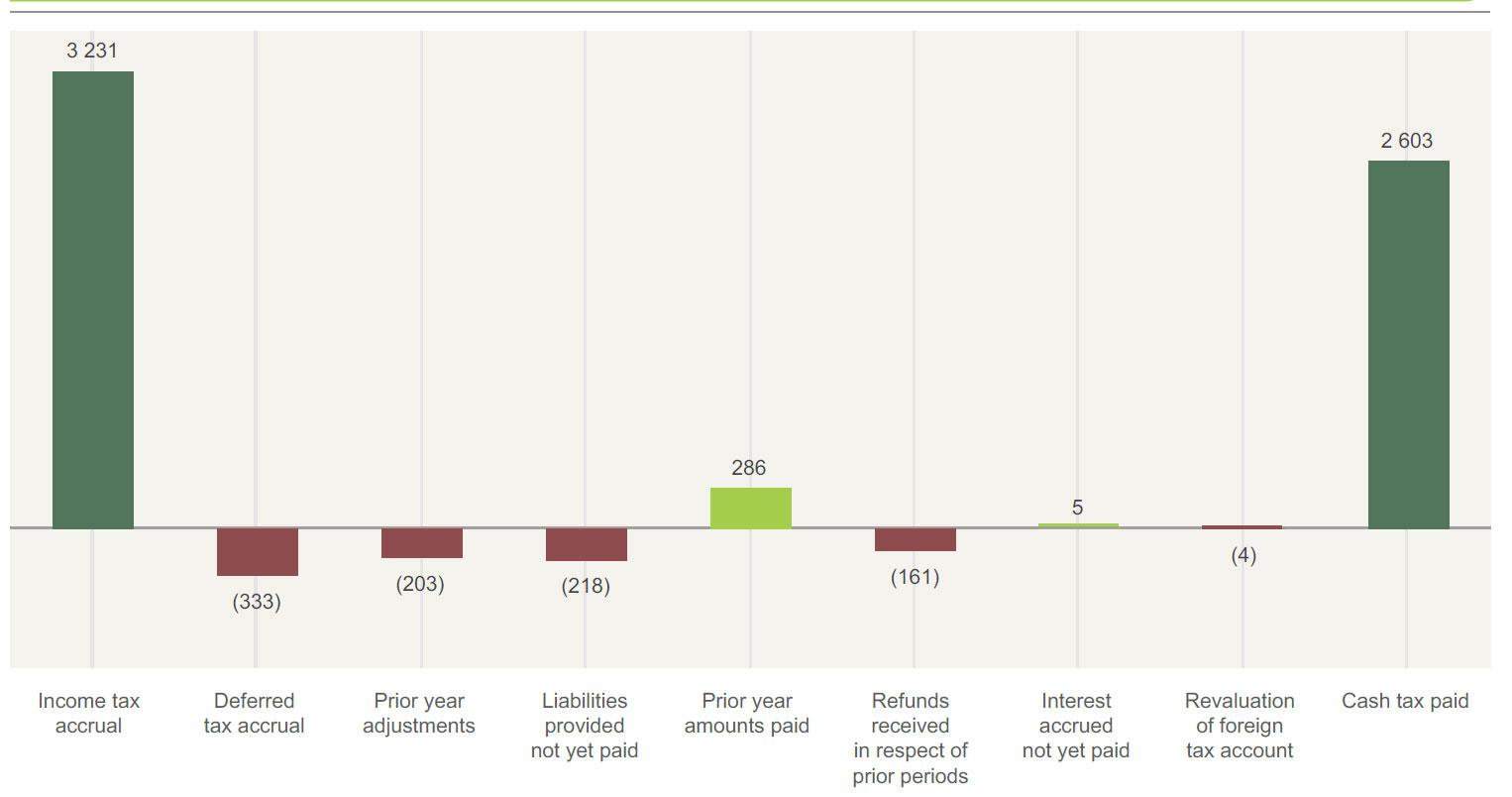

Reconciliation of tax accrual to cash tax paid (Rm)