Business risks and opportunities for growth

Exxaro has a mature risk management culture that forms part of our strategy, governance and day-to-day operations.

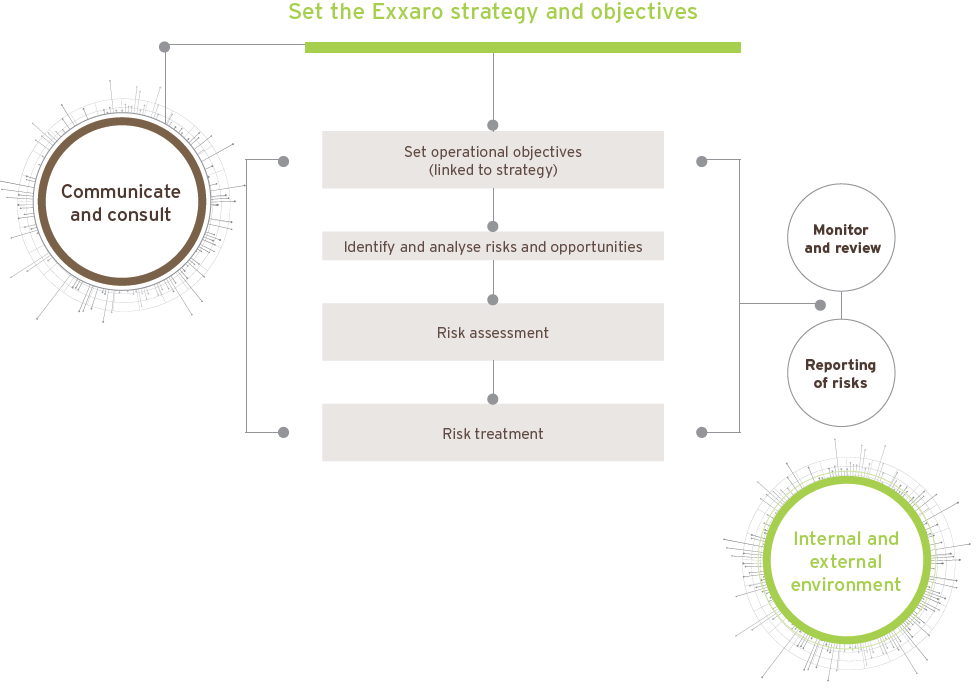

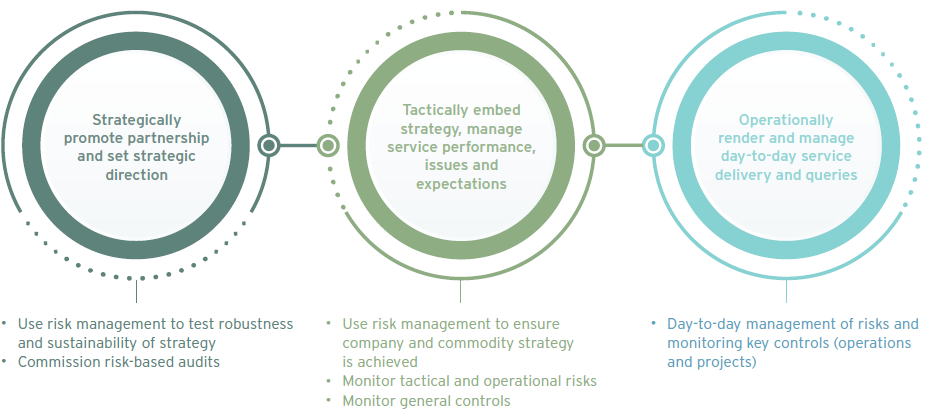

Risk management process

The Exxaro risk-management process is a strategic enabler embedded in all our processes, functions and systems. Risk management,

together with crisis management, is a board objective, which is ingrained in the Exxaro corporate culture.

The board and respective management layers consider business risks when setting strategies, and monitor controls continuously at

strategic, tactical and operational levels.

Risk management approach

The group’s risk management is mature. It is performed at management level with a different scope and context in mind. The layers

are vertically integrated and provide input into the specific risk profiles.

Risk appetite and thresholds

Exxaro defines risk appetite as the type and level of risk the group is willing to accept in order to meet strategic objectives.

We understand that, if we want to create value for all our stakeholders and remain sustainable, we need to measure and monitor our progress by using appropriate key performance indicators (KPIs).

The board and executive committee monitor KPIs quarterly to ensure all risks and key metrics are within Exxaro’s risk appetite. The KPIs and their thresholds are reviewed by the board and executive committee at least annually.

For details, please refer to performance against strategy.

For details, please refer to performance against strategy.

Pursuing opportunities

The Exxaro risk management framework also caters for the identification and realisation of opportunities, for example, early value coal extraction to maximise value in the short to medium term in view of the climate change risk. We believe that, for Exxaro to remain sustainable in the near future, it is important to adapt to change, and to identify and pursue possible opportunities that ultimately create value.

The opportunities we identified in 2019 are outlined in the table below.

| Opportunity |

|

Related material theme |

| Coal digitalisation journey: long-term improvement in productivity and cost |

|

Business resilience |

| Project XXX initiatives: short-term throughput improvements |

|

| Operational excellence drive: improvements in cost and throughput |

|

| Closing the gap initiatives: EBIT improvement towards 2023 target |

|

| Early value strategy: extract future value earlier |

|

| Liberating high-value product to maximise our product mix |

|

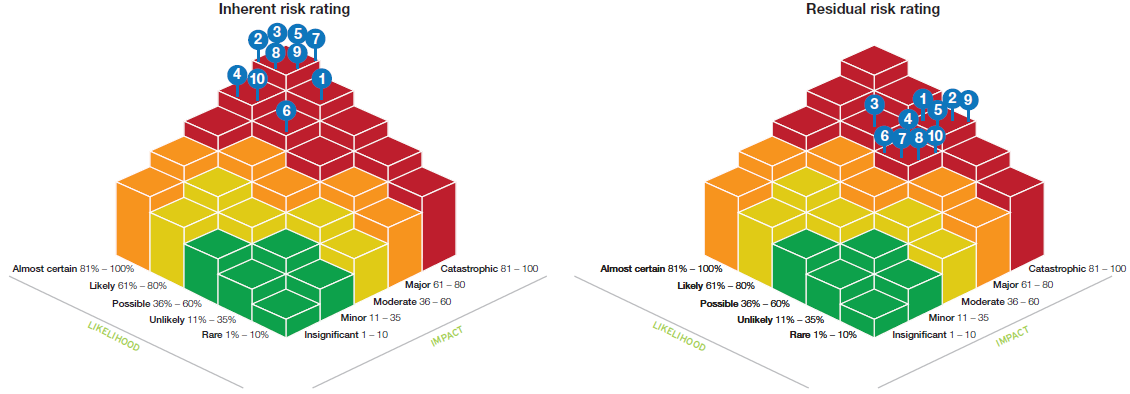

The formula indicates the universal assertion that risk is a function of likelihood and impact.

2019 vs 2018 risk comparison

Our risk scores are derived from the product of the likelihood and the impact of the eventuality. We rank our risks according to residual core risks from highest to lowest.

The following significant changes occurred in the past year:

- Climate change concerns increased significantly and moved from number 11 in 2018 to number 2 in 2019:

- Exxaro is facing intense scrutiny by consumers and activists demanding greater visibility and transparency with regard to carbon footprint and emissions reduction strategies. Shareholder activists are also driving coal miners to reshape their portfolios. Our climate change strategy (page 102) includes an impact risk assessment (in terms of physical and transitional risks) which will be conducted during 2020 to quantify and develop specific treatments for the business. As climate change shortens the lifespan of operations, we will focus on extracting the best quality coal (with high calorific or energy value). Production and mining plans will be amended accordingly to minimise the amount of coal extracted without compromising our contractual obligations. Due to pressure from investors and environmental lobbyists, there is limited capacity in the insurance market for fossil fuel companies. As such, this risk has a direct impact on our insurance portfolio. Going into the renewal period, the insurance market will be even more challenging. We may require recapitalisation of our insurance captive company in the event that full cover is not secured from the market for Exxaro’s insurance programme.

- Price and currency volatility risk was reassessed and separated into:

- Commodity price volatility

- Exchange rate volatility

- Safety and health risk increased to appear in the top 10:

- We had more than 6 000 additional temporary employees on our sites at the peak of our capital expansion programme. Consequently, due to the nature of mining, an increased number of employees and contractors were exposed to occupational risk. Due to the nature of mining, employees and contractors are exposed to occupational risk. Safety interventions have been introduced to reinforce the need to adhere to safety procedures, and to improve safety culture and behaviour.

Top 10 heat map

Exxaro’s top 10 risks are plotted inherently (before controls) and residually (after controls) on the heat map below, followed by an outline of our key identified risks, the main drivers, their potential impacts and mitigating treatments. We have considered internal and external risks, and our mitigation strategies depend on the severity of impact and likelihood of occurrence.

The pages that follow refer to the legends below:

| First line of defence |

Second line of defence |

Third line of defence |

| Management of risk – (risk owner) |

Management support and oversight |

Independent assurance |

Response strategy to risks and trends

We are pleased with the movement and direction of our risks during this past year. The extent of the shift is testament to the effectiveness of our response actions and has reflected in the success we achieved with our strategic objectives as described elsewhere. We are operating in an increasingly “VUCA” world, therefore as we manage some risks (and take advantage of opportunities) and succeed in our business strategy, so new risks and opportunities arise.

2. Climate change

Climate change has moved significantly up the risk ranking during 2019. Investor sentiment is increasingly bearish towards coal and Exxaro has engaged with several shareholders regarding our transition strategy.

1. Eskom systemic risk

The risk trend, given this exposure, remains top of the list, and the response requires strategic and policy changes for Eskom (and the electricity/energy industry).

3. Community unrest

This risk will remain heightened as we approach local government elections in 2021, where access to basic services, local employment and procurement may be in focus.

4. Commodity-price volatility

We are exposed to both coal and iron ore prices given our business structure, with both commodity prices having been impacted by an unprecedented number of unforeseen events, resulting in volatility. Exxaro’s export coal price is largely unhedged, taking full advantage of spot prices. Our iron ore exposure is through our passive investment in SIOC.

5. Cost competitiveness of products

This risk has been moved up the risk register due to the uncertainty and volatility within the environment in which we operate. Remaining cost competitive in an environment of price volatility is a key tenant of our operational excellence strategy.

6. Competition and product substitution

Renewables are becoming cheaper as a source of energy for electricity generation. In addition, we have witnessed the substitution of coal with gas in European markets as liquefied natural gas (LNG) prices dropped. Our proactive responses include continuing cost management to remain competitive (as described above) and exploring investment opportunities in renewables, which has resulted in a slight reduction in risk exposure.

7. Loss of social licence to operate

This risk is attributable both to the increasing regularity requirements from BEE-related legislation and impact on Exxaro’s reputation as a vehicle for social good. We have improved our BEE recognition level, from a level 5 to a level 2, indicating the transformative impact from our broad-based initiatives in terms of economic ownership; employment equity; skills development; enterprise and supplier development; and community development (including ESD). Our public relations and branding activities have increased presence on social media and earned a net positive sentiment.

8. Cybersecurity threats

As a result of increasing cyber threats globally, as well as our ongoing digitalisation strategy, cybersecurity has increased in ranking into the top 10.

9. Safety and health concerns

Our safety performance, as measured in terms of LTIFR has remained flat at 0.12 over the past three years, but above our target of 0.11. Safety risk has been moved up the risk register as a result of an increase in the temporary employment of contractors during our R20 billion expansion programme; which brings increased numbers of people onsite and therefore increased complexity.

10. Exchange-rate volatility

The exchange rate is affected from both domestic and global events beyond our control. The ZAR/US$ exchange rate continues to weaken on the back of domestic political and economic uncertainty as well as geopolitics. While this trend is favourable to our export revenue, the negative social consequences and impacts on medium to long-term investment decisions is a concern.

|

Capitals impacted |

|

|

|

|

Drivers

- Inadequate environmental financial provision at captive mines

- Rehabilitation fund shortfall at Matla

- Realisation of approved funding for capital requirements (Matla capital project programme)

- Further delays in the Eskom Medupi power station operating at full capacity

- Eskom liquidity risk: Eskom not honouring commercial rights and obligations as per coal supply agreements

|

|

|

Strategic performance KPI

B-BBEE contribution level, black ownership, SLP project delivery, capital project delivery, core operating margin, annualised return on capital employed, annual core HEPS and net debt to annualised EBITDA

( Year in review, Strategic performance dashboard) |

Impacts

- Cost of production becomes uncompetitive at Matla (lack of capital)

- Loss of revenue

- Reputational damage

- Cash flow constraints at Eskom resulting in late or no payment to Exxaro

- Operational constraints at Grootegeluk due to pit liberation impacts as a result of further Medupi power station delays or inability of Eskom to take contracted offtake

|

|

|

Treatments

- Enforcement of coal supply agreement and arbitration award in terms of environmental funding

- Capex funding to build siding to evacuate coal

- Temporary solution to load test train from Waterberg to Mpumalanga

- Top management and political interaction with ministers when required

- Ongoing discussions on the future of Matla

|

Outlook

- Eskom continues to face a tough operating and fiscal environment

- Expect significant progress in improving offtake for Medupi

- Active participation and planning with Eskom to extract coal from Waterberg

|

|

|

|

| Lines of defence: 1 and 2 |

| Materiality theme: |

|

|

|

| Risk trend: |

|

|

|

|

Capitals impacted |

|

|

|

|

Drivers

- Poor plant design unable to withstand extreme weather conditions

- Poor monitoring and reporting of climate change impacts

- Infrastructure vulnerabilities

- Lack of awareness of climate change impacts

- Increased NGO activism

- International and local investor negative sentiment towards fossil fuels

|

|

|

Strategic performance KPI

Reportable environmental incidents, carbon intensity, water intensity and rehabilitation funding adequacy of commercial mines, ex guarantees

( Strategic performance dashboard, Environmental liabilities and rehabilitation) |

Impacts

- Reputational damage

- Loss of licence to operate

- Financial loss (increased carbon tax among others)

- Environmental impacts

- Legal claims against heavy polluters

- Health and safety impacts on employees (increased occupational incident rate due to heat stroke and increase in skin cancer among others)

- Energy security and supply

- Loss of throughput

- Natural disasters

|

|

|

Treatments

- Raise awareness of climate change impacts

- Invest in appropriate technology to reduce own emissions

- Develop market intelligence on carbon pricing

- Embed climate change mitigations in design criteria for existing and new projects

- Engage government and other role players in industry to align on the transition to a low-carbon future

- Engage with regulator to anticipate policy changes

- Link performance reward system to emissions reduction

- Plan and embark on coal early value strategy to reduce stranded assets

- Develop renewable energy strategy to transition to lower carbon economy

- Adopted TCFD framework to engage with shareholders and other stakeholders

- Align with Paris Agreement

|

Outlook

- Invest in renewable energy initiatives

- Initiate work on determining science-based targets for climate change

- Continue with emission reduction

|

|

|

|

| Lines of defence: 1, 2 and 3 |

| Materiality theme: |

|

|

|

| Risk trend: |

|

|

|

|

Capitals impacted |

|

|

|

|

Drivers

- Dissatisfaction with local economic development initiatives

- Political agitation

- High unemployment rate

- Lack of service delivery by local government

- High demand for skills development, employment and local procurement

- Poor implementation of SLPs

- 2021 municipal elections

- Perceived slow transformation at operations

- Increased activism by communities

- Conduct of contractors (employment practices) Exxaro is seen as endorsing

- Fractured communities and competing interests

- Manipulation of information/community against Exxaro

- Lack of employment opportunities

- Lack of skills development opportunities

- Lack of procurement opportunities

- Poor communication of opportunities

- Poor service delivery by municipality

|

|

|

Strategic performance KPI

B-BBEE contribution level, black ownership and SLP project delivery

( Strategic performance dashboard, Communities) |

Impacts

- Production interruptions

- Negative media reports (reputation)

- Jobs/opportunities for sale (misrepresents Exxaro)

- Potential harm to mine employees and contractors

- Potential damage to mine equipment and property

|

|

|

Treatments

- Emergency response and crisis management plans

- Carve out opportunities

- Municipal capacity building

- Design and implement Impact Catalyst

- Enterprise and supplier development (including contractors)

- Build local, provincial and national political relationships

- Invest in non-mining skills development programmes

- Roll out bursaries/skills development programmes

- Roll out community engagement plans for proactive engagement (see KAM)

- Transparent and ongoing communication with communities

- Ensure emergency response plans are in place at all business units

|

Outlook

- Given the upcoming local government elections in 2021, we anticipate increased electioneering activities

- Continue to proactively engage communities and other stakeholders to manage relations

|

| Lines of defence: 1 and 2 |

| Materiality theme: |

|

|

|

| Risk trend: |

|

|

|

| 4 |

|

Commodity price volatility |

|

Capitals impacted |

|

|

|

|

Drivers

- European debt crisis (especially Brexit)

- Global and domestic economic slowdown

- Structural economic challenges in the US and trade wars

- Depressed local demand (closure of ArcelorMittal and Saldanha plants)

- Global resistance to fossil fuels

- Cost of renewable energy technology decreases

|

|

|

Strategic performance KPI

Capital project delivery, core operating margin, annualised return on capital employed, annual core HEPS and net debt to annualised EBITDA ( Strategic performance dashboard) |

Impacts

- Financial losses

- Difficult to forecast planning and budgets

- Feasibility of new projects (capital projects not achieving expected returns)

- Existing assets not achieving expected returns

|

|

|

Treatments

- Hedging capital commitments

- Impact of volatility frequently assessed in corporate model communicate to coal

- Improve speed of mine planning to match price volatility

- Negotiate long-term fixed-price contracts linked to currency

- Diversify away from thermal coal

- Adoption of market to resource model

- Focus on market intelligence in the coal sector

|

Outlook

- Uncertainty in the global market will continue to prevail

- After effects of the COVID-19 pandemic will have an adverse impact on commodity markets and result in lower coal prices

|

| Lines of defence: 1 and 2 |

| Materiality theme: |

|

|

|

| Risk trend: |

|

|

|

| 5 |

|

Cost competitiveness of products |

|

Capitals impacted |

|

|

|

|

Drivers

- Limited LoM

- Poor capital project execution

- Cost containment discipline not uniform across the organisation

- Inflationary pressures

- Deteriorating mining conditions (decreasing yield and increasing stripping ratio)

- Not meeting production volumes

- Volatility of exchange rate

- Commodity price decline

- Inaccurate financial modelling

- Higher fixed costs (headquarters costs are charged to the business units)

- South African geographical constraints

- Frequent changes in legislation (cost of licence to operate)

|

|

|

Strategic performance KPI

Core operating margin, annualised return on capital employed, annual core HEPS and net debt to annualised EBITDA

( Year in review, Strategic performance dashboard) |

Impacts

- Reputational damage

- Margin squeeze

- Premature mine closure and allocation of costs to other operations

- Reduced earnings

- Social impact

|

|

|

Treatments

- Assign management accountants as business partners in relevant areas

- Budget for post-production stoppage (rehabilitation cost)

- Create strategic joint ventures to optimise economies of scale

- Embrace technology and innovation to improve productivity

- Focus on sustainable cost reduction programmes and business improvement initiatives

- Focus on controllable efficiencies at business units

- Increase awareness of cost management

- Investigate and divest non-core and sub-par assets

- Optimise operating model and avoid duplicated activities

- Plan reviews by coal operations committee

- Rebalance product chains to improve infrastructure use (integrated logistics)

- Re-optimise capital in projects (mega projects and stay-in-business capital)

- Review and monitor performance of suppliers and service providers

|

Outlook

- Improve cost competitiveness of products in midst of suppressed commodity prices with emphasis on improving cost containment discipline, achieving production targets and productivity benchmark standards, and reducing fixed costs (specifically head office costs impacting cost per tonne produced)

|

| Lines of defence: 1 and 2 |

| Materiality theme: |

|

|

|

| Risk trend: |

|

|

|

| 6 |

|

Competition and product substitution |

|

Capitals impacted |

|

|

|

|

Drivers

- Regulatory push

- Price-driven substitution

- Advances in technology

- Pressure from stakeholders

- Environmental concerns

- Inability to grow coal and future material)

|

|

|

Strategic performance KPI

Growth strategy project delivery (CEO and executive committee performance contracts) ( Strategic performance dashboard, Remuneration report) |

Impacts

- Reputational damage

- Financial loss

- Loss of market share

|

|

|

Treatments

- Develop growth strategy and submit for board approval

- Early alerts about regulatory changes

- Implement diversification strategy

- Invest in cleaner coal-extraction alternatives

- Proactive engagement with stakeholders

- Target markets with dominant and growing coal consumption

|

Outlook

- Continuous reduction in costs of alternative sources increases threat of product substitution (finalising and implementing Exxaro’s strategy for a Just Energy Transition to renewables)

|

| Lines of defence: 1 and 2 |

| Materiality theme: |

|

|

|

| Risk trend: |

|

|

|

| 7 |

|

Loss of social licence to operate |

|

Capitals impacted |

|

|

|

|

Drivers

- Unable to achieve SLP targets as approved

- Increased social activism due to socio-economic challenges

- Increased state intervention in mining sector through legislation and regulation

- Depressed economic outlook

- Unable to meet some new mining charter targets (such as procurement)

- Onerous compliance requirements

- Lack of or limited communication

- Lack of understanding of collaboration principles by other stakeholders

- High expectations for social investments and procurement opportunities

- Delayed delivery of projects (not meeting community expectations)

- Delays in approval of licences and authorisations

|

|

|

Strategic performance KPI

B-BBEE contribution level, black ownership and SLP project delivery ( Year in review, Strategic performance dashboard) |

Impacts

- Community unrest

- Production stoppages and closure by communities

- Directives issued by Department of Mineral Resources and Energy as remedy

- Penalties and fines for non-compliance

- Adverse media exposure affecting reputation

- Suspension or cancellation of mining right

|

|

|

Treatments

- Adherence (as minimum) to new mining charter and B-BBEE requirements of Department of Trade and Industry

- Conduct SLP audits

- Proactive involvement in sustainable socio-economic development initiatives

- Timely implementation of SLPs

- Strengthen relationships with communities

- Increase effectiveness of human resource development programme

- Regular engagement with government

- Compliance performance management

|

Outlook

- Continue to drive delivery of SLPs

- Actively monitor regulatory environment to identify any change in compliance requirements and accordingly adapt compliance efforts

- Entrench efforts to improve stakeholder relations and align with their expectations

|

| Lines of defence: 1, 2 and 3 |

| Materiality theme: |

|

|

|

| Risk trend: |

|

|

|

|

Capitals impacted |

|

|

|

|

Drivers

- Large number of devices connected to corporate network requires management (security updates)

- Vulnerability due to lack of awareness

- People opening Exxaro up to attacks

- Greater vulnerability due to increased number of connected devices especially in operational systems

|

|

|

Strategic performance KPI

Capital project delivery ( Year in review, Strategic performance dashboard) |

Impacts

- Loss of production

- Loss of information

- Financial loss (ransom – increased cost and production loss)

- Business interruption

|

|

|

Treatments

- Ensure gaps are bridged between IT/OT

- Ensure that all devices are governed by company security policies

- Implement cloud security framework

- Upgrade of all network devices and PCs

- Effectively respond to attacks

- Ensure business continuity management plan in place and review regularly

|

Outlook

- Continuously monitor IT/OT environment to detect potential threats

- Continue to roll out cloud strategy

|

| Lines of defence: 1, 2 and 3 |

| Materiality theme: |

|

|

|

| Risk trend: |

|

|

|

| 9 |

|

Safety and health concerns |

|

Capitals impacted |

|

|

|

|

Drivers

- High/excessive fatigue levels

- Poor procedures for maintenance of equipment and machinery

- Inadequate on-the-job training due to illiteracy

- Lack of awareness of health risks

- Lack of hazard awareness (in line of fire)

- Non-adherence to procedures

- Lack of communication among teams working on equipment

- Lack of change management

- Design or modification of equipment without sign-off

- Inadequate supervision

|

|

|

Strategic performance KPI

Fatalities, LTIFR, OHIFR and skills provision( Year in review, Strategic performance dashboard) |

Impacts

- Fatalities and injuries

- Operational stoppages

- High insurance premiums

- Loss of licence to operate

- Decrease in quality of life

- Section 54/55 fines and penalties imposed by Department of Minerals and Energy

- Loss of productivity (deaths, medical incapacity or sick leave)

|

|

|

Treatments

- Analyse historic incident data to identify trends and root causes

- Consequence management applied consistently

- Continuous investigation and reporting of incidents

- Ensure implementation and maintenance of proximity detection systems

- Establish compliance-based committees to manage, educate and communicate

- Implement safety summit and indaba

- Implement safety, health, environment and community risk management tool

- Improve safety management with innovation

- Ensure PDS systems implemented and maintained

- Consequence management to be applied consistently

|

Outlook

- Implementation of the Khetha Ukuphepha campaign

- Focus on improving safety performa

|

| Lines of defence: 1, 2 and 3 |

| Materiality theme: |

|

|

|

| Risk trend: |

|

|

|

| 10 |

|

Exchange rate volatility |

|

Capitals impacted |

|

|

|

|

Drivers

- European debt crisis (especially Brexit)

- Social and political challenges in South Africa

- Structural economic challenges in the US

- Global economic slowdown

- Limited domestic demand may require additional exports with potentially negative financial impact due to exchange rate

|

|

|

Strategic performance KPI

Core operating margin, annualised return on capital employed, annual core HEPS and net debt to annualised EBITDA ( Year in review, Strategic performance dashboard) |

Impacts

- Financial loss (viability of business units)

- Difficult to conduct forecast planning

|

|

|

Treatments

- Hedging of capital commitments

- Impact of volatility frequently assessed in corporate model and communicated

- Difficult to conduct forecast planning and budget

- Improve speed of mine planning to match volatility (Wings strategy)

- Negotiate optimal Eskom contracts

- Placement of products (local versus export)

|

Outlook

- The World Economic Forum revised outlook for economic growth in 2020 and 2021: effect of slowing economic outlook has significant impact on emerging markets like South Africa with negative sentiment affecting the stability of the local currency

(exacerbated by country-specific challenges weighing on demand for local currency)

|

| Lines of defence: 1, 2 and 3 |

| Materiality theme: |

|

|

|

| Risk trend: |

|

|

|