Exxaro Resources Limited

Tax report for the year ended 31 December 2022

Exxaro's ERM framework considers today's uncertain operating environment in effective risk management to achieve our strategic objectives. Embedding risk management in existing processes is important for informed decisions and proactive planning. An effective approach to uncertainty and stakeholder expectations requires focus on TRM.

TRM includes operational risk management techniques, regulatory requirements for transparency and disclosure, a restrictive mindset in tax planning and a focus on good corporate governance. It is a proactive, systematic analysis of possible unwanted events and responses (including controls and treatment plans) rather than a reactive mechanism for detected events.

TRM is part of Exxaro's ERM structure to ensure the tax function's independence.

Although Exxaro views tax planning as a legitimate business lever within the parameters of tax legislation, the group has zero tolerance for evading any tax liability or facilitating the evasion of any tax liability on behalf of a third party. Exxaro has no appetite for transactions that have no valid commercial purpose other than obtaining a tax benefit. Exxaro avoids tax practices that are misaligned with its approach to tax and tax strategy.

Risk can be defined as the chance of an event occurring and impacting objectives. The objective of risk assessment is to identify, analyse and evaluate the impact of events and associated risks on the strategic objectives of the company. Analysing and assessing risks include estimating both the likelihood of events occurring as well as the impact, financial or otherwise, on the group.

Exxaro has identified the key activities that drive tax risk and documented standard operating procedures and controls to mitigate the identified risks.

The five top risks identified by the risk assessment process is captured in the ERM risk assessment and management tool - SAP GRC10.1 (SAP GRC). The SAP GRC allows group tax and the chief risk officer to monitor improvements and treatment plans.

It is important to keep the board, the audit committee, executive management and other internal and external stakeholders abreast of TRM activities.

The following TRM information will be reported:

| Type of information | Reporting responsibility |

Timing | Format of the report | Forum for discussion and evaluation |

| The initial formal TRM framework | Group tax manager assisted by TRM champion | Once off | TRM framework | Chief risk officer and chief financial officer |

| Feedback on the effectiveness of the TRM process | Internal audit department | Ad hoc | Internal audit reports | Audit committee |

| Feedback on changes to the TRM process | Group tax manager assisted by TRM champion | Significant changes are reported on an ad hoc basis | TRM memorandum | Chief risk officer |

| Identification of new risks with a moderate impact factor that has a possibility of occurring where controls are in place | Group tax manager and tax risk champion | Annual | As prescribed by the ERM framework | Chief risk officer |

| Unwanted events with an impact factor greater than 35% (thus a tax impact greater than R10 million – increased to R30 million from 2023) | Group tax manager and tax risk champion | Quarterly | Audit committee report | Executive committee and audit committee |

|

Our business risks and opportunities (IR) |

|

Stakeholder management (ESG report) and creating value through stakeholder engagement (IR) |

Risk can be defined as the probability of an event happening that will impact your objectives and it can be quantified as the:

Inherent risk does not consider any controls (except baseline controls, which are intrinsic to the hazard).

Residual risk is where the likelihood is reduced by controls that address the root cause and/or the trigger/driver of the unwanted event and, where the impact is reduced by controls, minimising those impacts.

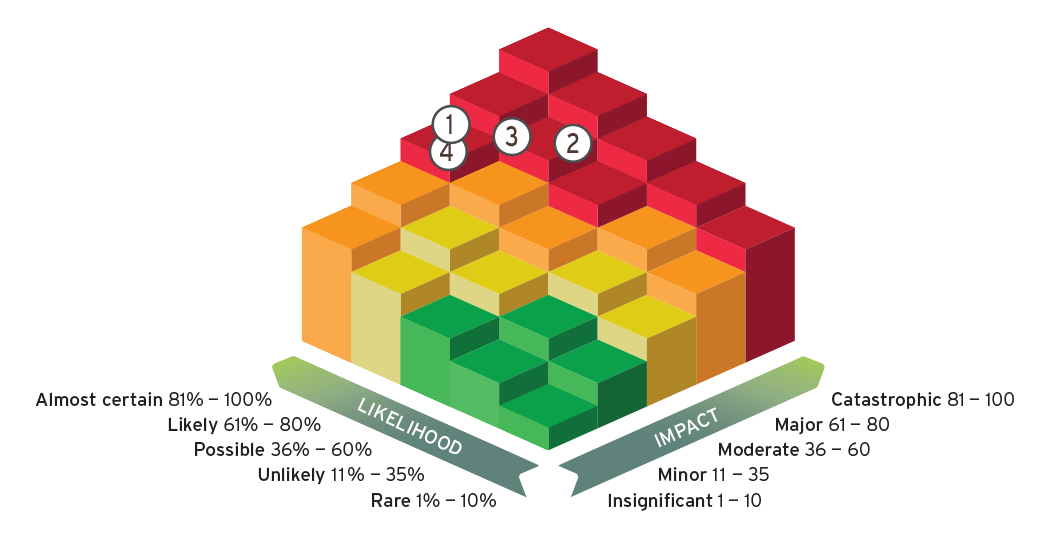

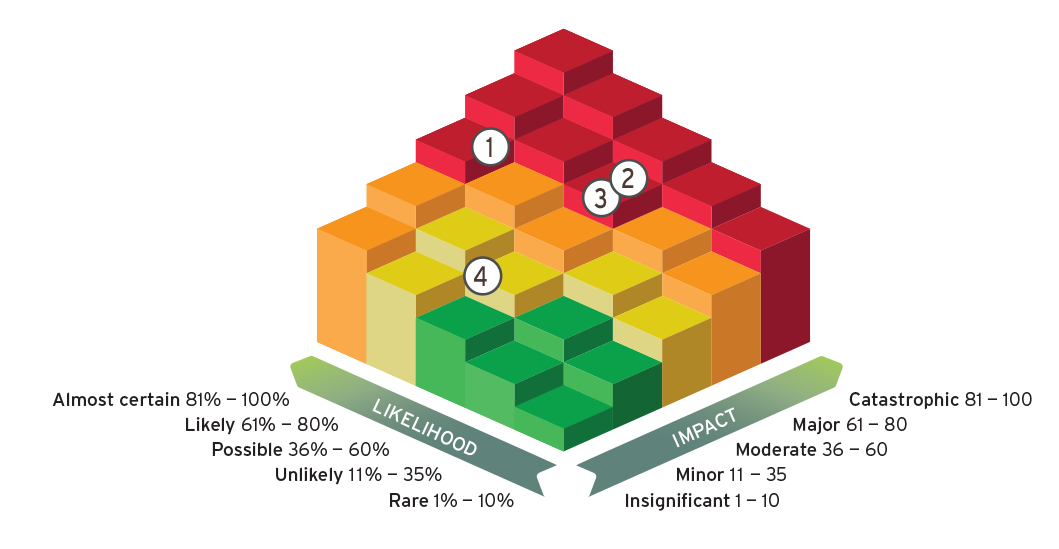

Risks are prioritised based on inherent risk, a predetermined risk appetite, the likelihood of the matter arising and its impact on value creation. Exxaro's top four material tax risks are discussed below.

These risks have been rated using the impact scales below which have been approved by the board in Exxaro's TRM policy. The impact scales for tax were specifically reduced from those set in terms of group ERM in line with Exxaro's reduced appetite for tax risks.

| Impact scale | ||

| Description | Indicator | % risk factor |

| Catastrophic | Tax impact >R75 million | 81 to 100 |

| Major | Tax impact >R50 million to R75 million | 61 to 80 |

| Moderate | Tax impact >R10 million to R50 million | 36 to 60 |

| Minor | Tax impact >R5 million to R10 million | 10 to 35 |

| Insignificant | Tax impact <= R5 million | <10 |

| Likelihood scale | ||

| Description | Indicator | % risk factor |

| Almost certain | Potential to occur every year | 81 to 100 |

| Likely | History of occurrence | 61 to 80 |

| Possible | Has occurred in the last five years and is expected to occur again | 36 to 60 |

| Unlikely | Theoretically possible | 10 to 35 |

| Rare | Very unlikely to occur and/or has not occurred to date | <10 |

The outcome of the ratings was as follows:

| Ranking | Risk name | Trend |

| 1 | Understatement of penalties for non-compliance |  |

| 2 | Tax and accounting disclosure differences | |

| 3 | Negative tax adjustments due to inability to supply documentary evidence |  |

| 4 | Cash flow constraints due to delay in obtaining tax clearance certificates | |

| 5 | Diesel refund audits not finalised |  |

|

The residual risk score decreased from the previous year |

|

The residual risk score stayed unchanged from the previous year |

| This is a new risk identified and did not exist in the previous year | |

|

This risk existed in the previous year but increased controls reduced the risk to insignificant levels, and it is no longer considered a risk |

1 |

Understatement of penalties for non-compliance | ||

| Drivers | Strategic performance KPIs | ||

| The scope of "prejudice" defined by the Tax Administration Act is broad with potential for inadvertent errors and non-disclosure | Core operating profit | ||

| Impacts | Treatments | ||

|

|

||

| Lines of defence | 1 and 2 |

2 |

Tax and accounting disclosure differences | ||

| Drivers | Strategic performance KPIs | ||

| International Financial Reporting Standards (IFRS) and tax law disclosures misaligned | Core operating profit | ||

| Impacts | Treatments | ||

|

|

||

| Lines of defence | 1 | ||

3 |

Negative tax adjustments due to inability to supply documentary evidence | ||

| Drivers | Strategic performance KPIs | ||

| Documentary evidence is not available as documents are retained for seven years in line with the Companies Act, 2008 (Act 71 of 2008), as amended, but SARS requests older information | Core operating profit | ||

| Impacts | Treatments | ||

|

Adherence to SARS requirements for tax submissions to ensure return prescription periods do not exceed the seven-year documentation retention period | ||

| Lines of defence | 1 and 4 | ||

4 |

Cash flow constraints due to delay in obtaining tax clearance certificates | ||

| Drivers | Strategic performance KPIs | ||

|

Core operating profit | ||

| Impacts | Treatments | ||

|

|

||

| Lines of defence | 1 | ||