Exxaro's manufactured capital is the physical mining, energy and property assets that enable us to deliver our products. The quality of our assets and how effectively we use them impact our overall value creation and operational performance.

We invest in our assets to maintain their enduring value, upkeep and performance, and optimise their use in delivering our products at optimal qualities. Optimising our portfolio and effectively using our invested capital enables us to achieve excellent operational performance, which in turn enables value creation and preservation across the other five capitals.

We deliver value through our:

We build momentum and resilience in executing on our strategy and business model through operational excellence and continued investment in our manufactured capital.

| Material theme | Matter | Supporting our strategy | Our broader impact |

changing context |

|

|

|

strategy |

|

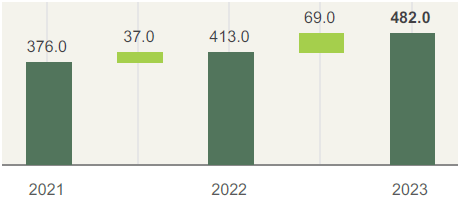

R2.5 billion

invested in sustaining capital (2022: R1.4 billion)

R0.2 billion

invested in expansion capital (2022: R0.3 billion)

R2.7 billion

invested in property, plant and equipment (2022: R1.7 billion)

Exxaro's operational performance areas encompass coal, energy, ferrous, portfolio optimisation and investments in minerals and energy.

Looking ahead

Safety, portfolio optimisation, cost efficiency and continuous business improvement remain our priorities across our coal and energy businesses.

International thermal coal pricing (API4) averaged US$121/t in 2023 (2022: US$271/t). Prices declined from 2023 levels due to coal to gas switching in Europe. Europe and key markets in Asia also remained well stocked during the year, keeping prices stable.

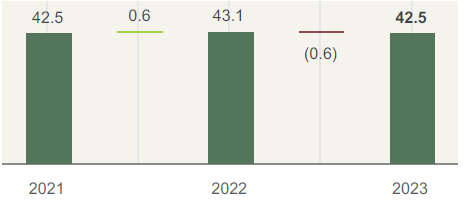

Production cost per tonne was mainly impacted by lower offtake, resulting in increased total tonnes handled with the following impact on costs:

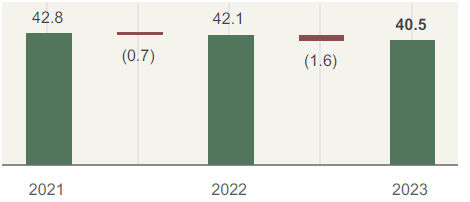

These costs were offset somewhat by the decrease in the rehabilitation liability mainly due to an increase in discount rates.

Other operational costs were impacted by a net positive foreign exchange variance due to a weaker ZAR/USD exchange rate on revenue as well as realised and unrealised foreign exchange differences on foreign debtors and cash balances. Royalties decreased in line with lower revenue, while our insurance expense also decreased due to the change in accounting treatment of new insurance products. These decreases resulted in a premium expense (classified as a financial asset) on the balance sheet.

Our net cash cost per tonne was above mining inflation, impacted by increased cost as explained. However, our cost per total tonnes handled was R1 lower, demonstrating our ability to cost-efficiently move volumes.

In the face of a challenging macro-environment, our commitment to cost containment remains. We therefore see ourselves returning to normalised cost as we bolster our responsiveness to a new, ongoing reality.

Cennergi's operational EBITDA margin was 80% (2022: 80%), showing the consistency of earnings underpinned by long-term offtake agreements.

The two windfarms generated 727GWh in 2023 (2022: 671GWh), despite the Tsitsikamma community windfarm suffering 15GWh of losses owing to an Eskom distribution line fault. The increase in generation resulted from improved wind conditions. Our average equipment availability was 97.3% in 2023, slightly above the contracted levels of 97.0%.