| |

Revenue | EBITDA1 | |

||||

| |

2024 Rm |

2023 Rm |

% change |

2024 Rm |

2023 Rm |

% change |

|

| Coal | 39 115 | 36 945 | 6 | 10 236 | 12 213 | (16) | |

|---|---|---|---|---|---|---|---|

| Energy | 1 411 | 1 345 | 5 | 1 031 | 1 023 | 1 | |

| Ferrous | 190 | 398 | (52) | (45) | 83 | (>100) | |

| Other2 | 9 | 10 | (10) | (799) | 80 | (>100) | |

| Total | 40 725 | 38 698 | 5 | 10 423 | 13 399 | (22) |

| 1 | EBITDA is calculated by adjusting net operating profit before tax with depreciation, amortisation, impairment charges or impairment reversals, and net losses or gains on disposal of assets and investments (including translation differences recycled to profit or loss). Refer to note 3.3 for key numbers used in the calculation of EBITDA. |

| 2 | Relates mainly to the corporate office and smaller operations. |

Group revenue increased by 5% to R40 725 million (2023: R38 698 million), primarily due to a 6% increase in coal revenue driven mainly by higher coal export volumes and higher prices in the domestic market, and a 5% increase in energy revenue.

Group EBITDA declined by 22% to R10 423 million (2023: R13 399 million), mainly attributable to a 16% decrease in coal EBITDA and a negative contribution from the other operating segment, which is discussed further under each business segment.

| Equity-accounted income/(loss) | Dividends received | ||||||

| 2024 Rm |

2023 Rm |

% change |

2024 Rm |

2023 Rm |

% change |

||

| Coal: Mafube | 234 | 508 | (54) | 130 | 1 525 | (91) | |

|---|---|---|---|---|---|---|---|

| Coal: RBCT | (7) | (10) | 30 | ||||

| Ferrous: SIOC1 | 3 979 | 6 157 | (35) | 3 741 | 3 386 | 10 | |

| Other: Black Mountain | 64 | 332 | (81) | ||||

| Total | 4 270 | 6 987 | (39) | 3 871 | 4 911 | (21) | |

| 1 | Includes Exxaro's share of SIOC's impairment reversal on mining assets, amounting to R596 million. The impairment reversal was due to a life of mine extension based on revisions to the forecast production volume profile. |

Headline earnings decreased by 36% to R7 298 million (2023: R11 327 million), mainly driven by the 22% decrease in group EBITDA and a 39% decrease in equity-accounted income. SIOC’s equity-accounted income declined by 35%, mainly due to lower iron ore prices and lower sales volumes, partially offset by the effects of an impairment charge reversal. Mafube’s equity-accounted income declined by 54%, owing largely to lower coal export prices.

The weighted average number of shares remained unchanged at 242 million, translating into a headline earnings per share of 3 016 cents per share (2023: 4 681 cents per share).

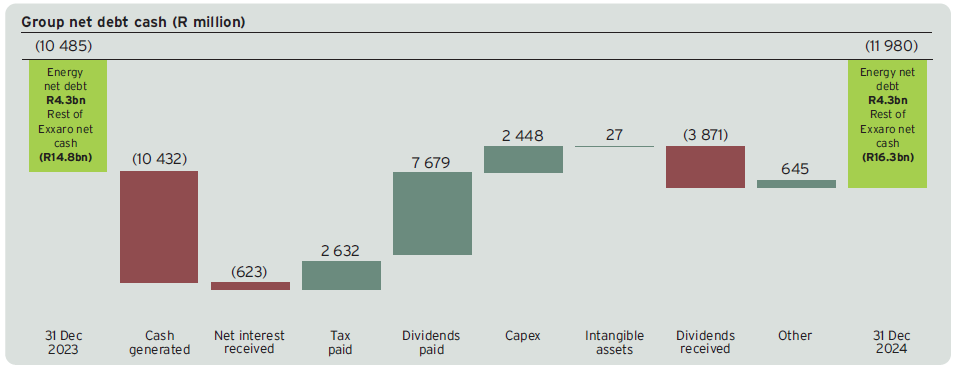

Cash generated by our operations amounted to R10 432 million (2023: R13 307 million), and dividends received from our equity-accounted investments totalled R3 871 million (2023: R4 911 million). These cash inflows were sufficient to cover our capital expenditure, taxation, and ordinary dividends paid.

Total capex decreased by 8% to R2 475 million (2023: R2 699 million). The capex for 2024 comprised R2 146 million, mainly for coal sustaining capital, R302 million expansion capital for our energy projects and R27 million intangible assets.

Our good cash generation increased our net cash position to R16 309 million (excluding energy’s net debt) as at 31 December 2024, compared to a net cash position of R14 834 million at 31 December 2023.

The coal market started on a bearish note in the first quarter of 2024 following trends from late 2023. This was primarily due to sufficient coal supply in key markets such as India, Japan, South Korea, and Taiwan, with lower gas prices, making gas a more competitive alternative in Europe. However, geopolitical factors played a significant role in lifting prices higher, alongside the TFR derailment in the first quarter of 2024 and early in the second quarter of 2024.

The resurgence in Indian demand was primarily maintained due to its strong economic growth, despite a brief decline between July and September 2024 due to high stockpiles of South African coal, the monsoon season, low domestic coal prices, and low steel prices. European demand faced headwinds from strong renewable energy generation, revision of coal phase-out targets and cheaper gas prices.

Japanese and South Korean demand remained steady, with Japan continuing to benefit from a diverse energy mix (gas, renewables, nuclear, and coal), but the restart of several nuclear plants posed a risk to coal demand.

The benchmark API4 RBCT export price averaged US$105 per tonne in 2024, compared to US$121 per tonne in 2023, a decline of 13%.

The South African domestic market demand remained resilient in the second half of 2024 despite macro-economic impacts affecting domestic end users. In the Waterberg region, Eskom’s coal offtake improved slightly, but operational challenges at power stations continued to impact its ability to consistently take coal from our Grootegeluk mine.

Rail operations continued to face ongoing disruptions, including cable theft, vandalism, unavailability of locomotives and wagons and infrastructure degradation. Additionally, three derailments affected TFR volume throughput in the first half of 2024. Despite these challenges and rail execution volatility, TFR’s performance to the Richards Bay Coal Terminal improved, increasing to 51.9Mtpa (2023: 47.9Mtpa), with a better performance recorded in the second half of 2024.

Coal revenue increased by 6% to R39 115 million in 2024 compared to R36 945 million in 2023. The higher revenue was mainly due to higher export volumes, albeit at a lower realised average export price of US$100 per tonne (2023: US$117 per tonne). Despite the price decline, Exxaro achieved a strong 95% price realisation in 2024 compared to 97% in 2023 owing to our effective market-to-resource optimisation initiatives. Higher domestic sales prices were not sufficient to offset the lower domestic volumes.

However, we also experienced cost pressures driven by inflation, higher selling and distribution costs due to the use of alternate distribution channels, and increased operational and maintenance cost, primarily driven by higher volumes of overburden.

| 2024 Rm |

2023 Rm |

% change |

|

| Sustaining | 2 080 | 2 433 | (15) |

|---|---|---|---|

| Commercial – Waterberg | 1 812 | 2 217 | (18) |

| Commercial – Mpumalanga | 268 | 201 | 33 |

| Other | 15 | (100) | |

| Total coal capex | 2 080 | 2 433 | (15) |

The coal businesses capex decreased by 15%, driven by lower sustaining capital spend at Grootegeluk for the Backfill phase 3 and the timing of the haul track replacement strategy.

Equity-accounted income from Mafube decreased by 54% to R234 million compared to R508 million in 2023, mainly due to lower coal export prices.

Cennergi’s operating wind assets generated 725GWh of electricity (2023: 727GWh), with revenue increasing by 5% to R1 411 million (2023: R1 345 million).

Cennergi’s EBITDA margin on the operating wind assets remained consistent at 80% (2023: 80%), underpinned by the long-term offtake agreements with Eskom.

Construction of the 68MW Lephalale Solar Project at Grootegeluk mine is ongoing, with commercial operations anticipated to start in mid-2025.

Cennergi’s operating wind assets project financing of R4 073 million (2023: R4 348 million) will be fully settled by 2031, while the LSP project financing of R1 150 million (2023: R477 million) will be fully settled by 2042. The project financing has no recourse to the Exxaro balance sheet and is hedged through interest rate swaps.

On 17 February 2025, Cennergi Holdings , a wholly owned subsidiary of Exxaro, in partnership with G7 Renewable Energies Proprietary Limited, reached financial close on the 140MW Karreebosch Wind Farm (RF) Proprietary Limited (Karreebosch) project. Karreebosch has a 20-year Power Purchase Agreement with Northam Platinum Limited. Cennergi Holdings acquired 80% of the share capital in Karreebosch as well as 50% of the share capital in Karreebosch Asset Management Proprietary Limited. The total investment cost of the project is anticipated to be R4.7 billion which will in majority be funded with project financing from Nedbank, Absa Bank, and Standard Bank with the financial structure set up to ensure long-term sustainability, as well as with limited recourse to the Exxaro balance sheet.

The Ferrous business comprises of the FerroAlloys operation. Due to lower offtake from customers, production was curbed to manage full stockpiles, resulting in an EBITDA loss of R45 million, compared to an EBITDA profit of R83 million in 2023.

Exxaro has made significant progress in disposing of our entire shareholding in Exxaro FerroAlloys Proprietary Limited, with the signing of a sale and purchase agreement expected to be concluded in 2025.

The 35% decrease in equity-accounted income from SIOC to R3 979 million (2023: R6 157 million) was driven by lower iron ore prices and sales volumes, partially offset by the effects of an impairment charge reversal.

In August 2024, we received an interim dividend of R1 634 million from our investment in SIOC. In February 2025, SIOC declared a final dividend to its shareholders. Exxaro’s share of the dividend amounts to R1 732 million, which is R98 million higher than the interim dividend received. The dividend will be accounted for in the first half of 2025.

The other segment mainly comprises costs related to the corporate office and smaller operations. The other operating segment reflected an EBITDA loss of R799 million (2023: R80 million EBITDA profit). The key reasons for the variance are:

The R268 million decrease in equity-accounted income from Black Mountain to R64 million (2023: R332 million) was mainly due to production challenges resulting in lower production and sales volumes.

To deliver on our strategic objectives of people empowered to create impact, reach carbon neutrality by 2050 and becoming a catalyst for economic growth and environmental stewardship, we incorporate responsible and sustainable business practices in everything we do. Not only do we aim to mitigate and manage our negative impact on natural resources, but we also contribute to enhancing ecosystem resilience and the lives of our employees and communities.

Our safety goal is to achieve Zero Harm by proactively managing safety priorities through the consistent implementation of Exxaro’s five safety focus areas. These are incredible safety leadership, effective communication, training, zero tolerance and risk management.

At the end of the financial year, the group completed 28 consecutive months without work related fatalities. This is a significant milestone, not only highlighting the effectiveness of our strategy but also the dedication and commitment of all our employees to safety. Other notable fatality free years reached are:

We were honoured to be recognised at the 2024 Coal Safe Awards, which celebrate the efforts of the coal mining industry in upholding safety standards. Amongst other awards received, Exxaro won the 2024 Best in Class Safety Record award.

Our LTIFR for the group of 0.06 in 2024 was an improvement compared to 0.07 per two-hundred thousand man-hours worked in 2023. Our target remained at 0.05.

We continue to drive safety, remaining vigilant to prevent workplace incidents, and fostering a proactive safety culture that safeguards lives and enhances operational resilience. In line with this commitment, we will be rolling out our refreshed safety strategy and embedding it across the group during 2025.

Our people are at the heart of everything we do. Exxaro is championing diversity, equity and inclusion and has maintained its value proposition as an employer of choice.

As such, Exxaro has once again received recognition from the Top Employer Institute as a 2025 Top Employer, achieving exceptional performance in areas of business strategy, diversity, equity and inclusion, people strategy, and for our listening strategies.

In 2024, we invested over R400 million to develop our people through comprehensive training programmes, leadership development initiatives and opportunities for continuous learning.

In 2024 we also signed a new three-year wage agreement with all trade unions, demonstrating the existence of strong relations built on trust and mutual respect.

Climate change remains a priority for Exxaro, and we remain committed to lowering our carbon footprint, especially in a fast-changing legislative environment.

Our Decarbonisation Roadmap, which was approved by the board, comprises a comprehensive framework that summarises our key milestones and strategic initiatives necessary for Exxaro to achieve carbon neutrality by 2050. From a 2022 base, we are targeting 40% and 75% cumulative reduction in scope 1 and 2 emissions, in 2030 and 2040 respectively. We will achieve this through renewable energy initiatives as well as equipment and fleet optimisation technology.

In 2024, we achieved carbon intensity of 4.12tCO2 e/kt TTM against our target of 4.2tCO2 e/kt TTM. This is an improvement of 6.4% from the 2023 carbon intensity of 4.4tCO2 e/kt TTM. Our water intensity of 142 l/t RoM was also within our 180 l/t RoM target, despite an increase from 105 l/t RoM recorded in 2023.

Our mine plans consider land management, mine closure and concurrent rehabilitation supported with financial provisions to ensure we honour our commitments. At the end of the financial year, our efforts on rehabilitation continued as we rehabilitated 477 hectares of disturbed land, increasing our rehabilitated land to 26% from 19% in 2023.

Encouragingly, we recorded zero level 2 and 3 environmental incidents during 2024. As catalysts for economic growth and environmental stewardship, we continue to explore strategic partnerships, adopting green technologies, and employing robust environmental management tools to drive continuous improvement and enhance sustainability.

Exxaro is committed to safeguarding biodiversity through targeted initiatives, including species relocation, wetland rehabilitp tion, invasive plant management, and implementing conservation programmes that protect the native flora and fauna across our operations. Our impacts on biodiversity are further enhanced by strategic partnerships with conservation organisations and communities.

Delivering meaningful socio-economic value is integral to Exxaro’s purpose of powering better lives in Africa and beyond. Our efforts focus on addressing unemployment, enhancing education, and enabling infrastructure development to empower host communities and drive inclusive economic growth.

As at 31 December 2024, social investments amounted to R2.1 billion, of which R28 million was social investment spend by Cennergi, benefiting socio-economic development initiatives including education, welfare, agriculture development, and health. The group’s local procurement from black SMME supported 562 SMMEs through enterprise and supplier development initiatives in 2024.

We are making a meaningful impact in our host communities by investing in education. Our early childhood development programmes benefited more than 2 700 children, more than 40 registered early childhood development centres, and more than 180 teachers through professional training. We also successfully connected 27 schools in Mpumalanga and Limpopo with wi-fi networks and provided information and communications technology labs to 20 schools.

In January 2025, Exxaro handed over the newly built Martina Kekana school hall, a block of four classrooms and associated external upgrades to Nelsonskop Primary school in Lephalale, benefiting more than 1 580 children and teachers. At an investment of R20.3 million, the project boosted the local economy, through local company participation and job creation.

The group has consistently maintained that when determining the level of dividend pay-out and, therefore, the dividend cover, cognisance needs to be taken of the current state of the industry, Exxaro’s capital expenditure requirements, and other relevant commitments. This is particularly relevant in the challenging economic environment, including the impact of the logistical challenges.

The board of directors has declared a final cash dividend comprising:

Notice is hereby given that a gross final cash dividend, number 44 of 866 cents per share, for the year ended 31 December 2024, was declared from income reserves and is payable to shareholders of ordinary shares on 12 May 2025.

For details of the final dividend, please refer to note 5.5. The details will also be published on our website at www.exxaro.com.

| Salient dates for payment of the final dividend are: | |

| Last day to trade cum dividend on the JSE | Tuesday, 6 May 2025 |

| First trading day ex-dividend on the JSE | Wednesday, 7 May 2025 |

| Record date | Friday, 9 May 2025 |

| Payment date | Monday, 12 May 2025 |

No share certificates may be dematerialised or re-materialised between Wednesday, 7 May 2025 and Friday, 9 May 2025, both days inclusive. Dividends for certificated shareholders will be transferred electronically to their bank accounts on the payment date. Shareholders who hold dematerialised shares will have their accounts credited at their central securities depository participant or broker on Monday, 12 May 2025.

Given the net cash position at 31 December 2024 of R16 309 million (excluding energy net debt), in addition to the final dividend declared, the board has approved a R1.2 billion share repurchase programme, subject to prevailing market conditions, and JSE Listings Requirements.