We build momentum and resilience in executing our strategy and business model through operational excellence and ongoing investment in our manufactured capital.

Exxaro's manufactured capital includes the physical mining, energy and property assets that enable us to deliver our products. The quality of our assets and how effectively we use them impact our overall value creation and operational performance. Our assets comprise five mines (including one JV), two coal projects, one ferro-silicon manufacturing facility, two windfarms in operation and one solar project under construction.

We invest in our assets to maintain their enduring value, upkeep and performance, while optimising their use to deliver our products at optimal qualities. Optimising our portfolio and effectively using our invested capital enables us to achieve excellent operational performance, which in turn enables value creation and preservation across the other five capitals.

| Material theme | Matters | Strategies to achieve our objectives | Related strategic objective |

Our broader impact |

Adapting to a changing context |

|

|

|

|

Executing our strategy |

|

|

|

|

Effectively and efficiently delivered coal to our customers at optimal value for both parties through process improvements and delivering stakeholder value

Achieved an 80% operational EBITDA margin and met generation targets with 725GWh produced, supported by high equipment availability and good wind conditions

Received dividends amounting to R3.7 billion from our investment in SIOC. The 45% decrease in adjusted equity-accounted income from SIOC to R3.4 billion (2023: R6.2 billion) was driven by lower iron ore prices and sales volumes

We made progress in executing our energy transition minerals diversification strategy, with several transactions at a matured stage, demonstrating our commitment to a sustainable future

We remain focused on safety, portfolio optimisation, cost efficiency and continuous improvement across

our coal and energy solutions businesses.

Exxaro developed a minerals business approach to support the transition to a low-carbon world while leveraging our core competencies in mining and logistics. Comprehensive screening criteria guide this approach to identify key energy transition minerals, positioning Exxaro for future growth.

Our early value strategy focuses on optimising Coal Reserves to minimise the risk of stranded high-value assets and enhance operational cost efficiency. At the same time, our market to resource optimisation strategy integrates market insights into operational planning to produce coal products that meet customer specifications and evolving market demands.

By aligning these strategies, we strengthen our ability to balance immediate energy needs with long-term sustainability, reinforcing our role in advancing energy security and driving a low-carbon future.

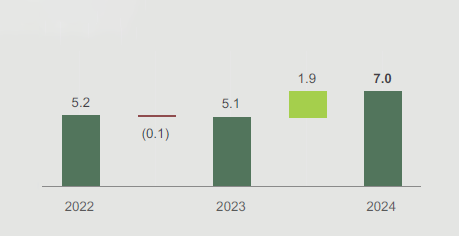

Total product (Mt)

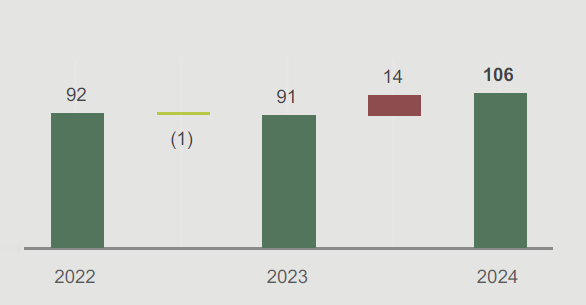

Total sales (Mt)

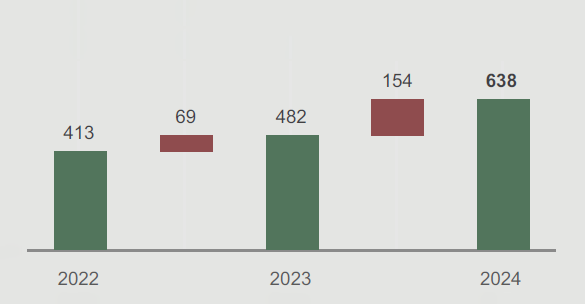

Export sales (Mt)

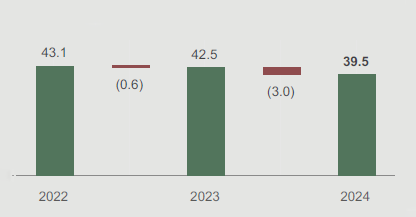

Cash cost per total tonnes handled (R/t)

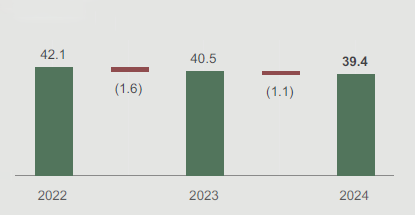

Cash cost per production tonne (R/t)

International thermal coal pricing (API4) averaged US$105/t in 2024 (2023: US$121/t). Prices declined from 2023 levels due to coal to gas switching in Europe, which was supported by improved gas and liquefied natural gas availability at lower pricing. High coal and gas inventories in Europe, Japan, Korea and Taiwan resulted in low spot coal demand. Milder temperatures in the northern hemisphere and good renewables performance also contributed.

In line with our market to resource optimisation strategy, production was mainly impacted by demand. However, export sales performed well, with an increase of 37%. The lower offtake continues to impact cost per tonne. Cost optimisation remains a pivotal element in achieving operational efficiencies, ensuring resources are utilised effectively and performance aligns with our goals. Total volumes handled increased in line with the expected mining geographical landscape from the various BUs.

Increased cost impacts are as follows:Our net cash cost per tonne was above mining inflation, primarily due to lower volume offtake and related increased costs. However, these increased costs supported business continuity and were offset by exceptional exports through alternative ports.

Our EBITDA decreased by 16% due to a decrease in the API4 price and the increased costs mentioned above. This was offset by positive impacts from higher export product sales.

Against a challenging macro-environment, we remain committed to cost containment. We anticipate returning to normalised costs as we bolster our responsiveness to an ongoing changing reality.

Cennergi's 2024 operational EBITDA margin was 80% (2023: 80%).

The two windfarms generated 725GWh (2023: 727GWh) during the year, which is in line with generation targets. Our average equipment availability was 96.2% due to various component replacements.