R38.7 billion Revenue, down 17% from R46.4 billion

R13.4 billion EBITDA, down 29% from R19.0 billion

R46.81 per share Headline earnings, down 22% from R60.16 per share

R13.3 billion Cash generated by operations, down 29% from R18.9 billion

R10.10 per share Final dividend

R5.72 per share Special dividend

Group revenue decreased by 17% to R38 698 million (2022: R46 369 million), mainly driven by significantly lower coal export sales prices achieved as a result of the steep decline in the API4 index price, partially offset by a weaker exchange rate and higher prices achieved on domestic sales.

Headline earnings decreased by 22% to R11 327 million (2022: R14 558 million), driven by the 29% decrease in group EBITDA, partially offset by an 8% increase in equity-accounted income. SIOC's equity-accounted income was 51% higher due to higher iron ore prices and sales volumes as well as cost-optimisation initiatives and as a result of the prior year including an impairment charge recognised on mining assets. This was partially offset by a 73% decrease in Mafube's equity-accounted income resulting mainly from lower export prices.

The weighted average number of shares of 242 million remained unchanged translating into headline earnings per share of 4 681 cents per share (2022: 6 016 cents per share).

Refer note 5.3 for the detailed reconciliation of headline earnings.

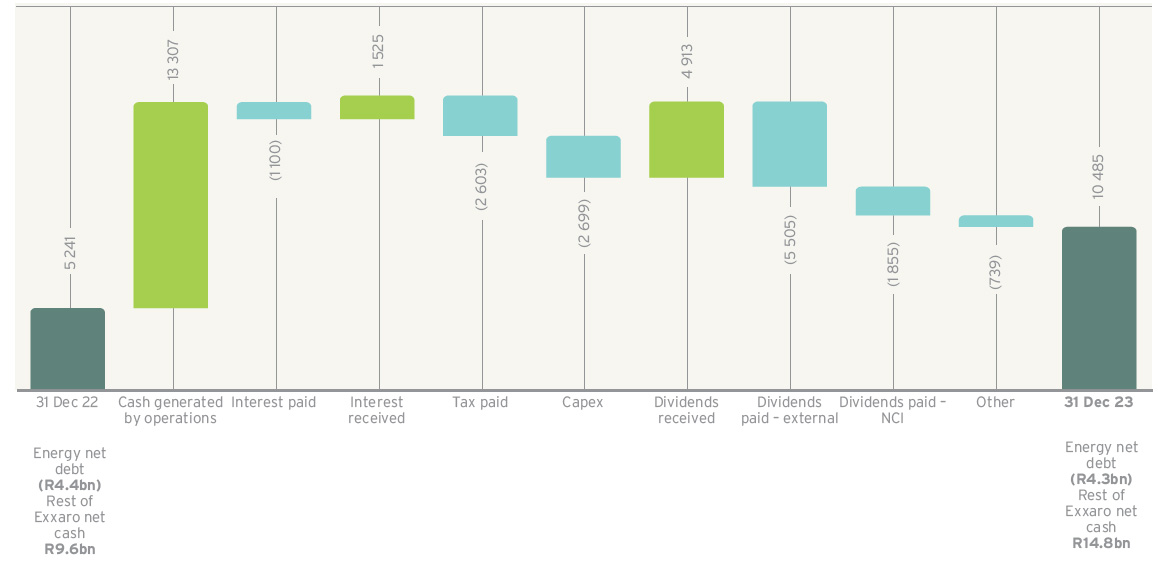

Cash generated by operations of R13 307 million (2022: R18 863 million) together with the dividends received from our equity-accounted investments of R4 911 million (2022: R5 903 million), were sufficient to fund capital expenditure, taxation, and ordinary dividends paid.

Total capex increased by 63% to R2 699 million (2022: R1 652 million). The capex for 2023 comprised R2 455 million sustaining capital and R244 million expansion capital.

Strong cash generation resulted in an increase in the net cash position to R14 834 million (excluding energy's net debt) compared to a net cash position of R9 645 million (excluding energy's net debt) on 31 December 2022.

The 2023 financial year has been characterised by declining coal prices due to a decrease in high Calorific Value coal demand, driven by sufficient gas and coal stocks in Europe, Japan, Korea, and Taiwan. The reduction in coal demand was exacerbated by warmer than usual winter temperatures, robust performance in renewable and nuclear energy generation, and significantly lower gas prices.

There was a resurgence in Indian demand compared to 2022, due to lower coal prices. In addition, changes in global trade flows were visible as Australia resumed supply into China from a previous trade ban, and Russian supplies to Europe and Japan reduced drastically, with Korea adopting a gradual approach of weaning itself off Russian coal.

China and India's economic growth and buoyant power demand were the main drivers for coal demand.

Domestically, operational challenges and equipment failures at Eskom's power stations impacted on the offtake of power station coal in the Waterberg region. The operating environment for domestic coal end-users was challenging in 2023 as a result of loadshedding, logistical challenges, slowing growth and inflationary pressures.

The benchmark API4 RBCT export price averaged US$121 per tonne (2022: US$271 per tonne). The group realised an average export price of US$117 per tonne (2022: US$251 per tonne). Despite this price decline, Exxaro was able to realise 97% of the average API4 index price based on its sales mix. Export volumes decreased slightly to 5.1 Mt (2022: 5.2 Mt).

Coal revenue decreased by 18%, driven by a decrease in revenue from the commercial mines due to lower export prices and volumes. Higher domestic prices were offset by lower domestic volumes.

The coal business's capex increased by 52%, driven by higher sustaining capital spend at Grootegeluk for the Backfill phase 3 and the equipment replacement strategy.

| 2023 Rm |

2022 Rm |

Change % |

|

| Sustaining | 2 433 | 1 374 | 77 |

|---|---|---|---|

| Commercial – Waterberg | 2 217 | 1 117 | 98 |

| Commercial – Mpumalanga | 201 | 252 | (20) |

| Other | 15 | 5 | >100 |

| Expansion | 231 | (100) | |

| Commercial – Waterberg | 231 | (100) | |

| Total coal capex | 2 433 | 1 605 | 52 |

Equity-accounted income from Mafube decreased by 73% to R508 million (2022: R1 902 million), mainly due to lower export prices.

Energy revenue increased by 16% to R1 345 million (2022: R1 159 million).

Cennergi's operating wind assets generated 727 GWh of electricity for 2023 (2022: 671 GWh). This is an 8% increase from the prior year due to improved wind conditions, despite the 15 GWh generation loss at one of the wind assets due to an Eskom distribution line fault that occurred earlier in the year.

Cennergi's EBITDA margin on the operating wind asset was consistent at 80% (2022: 80%) underpinned by the long-term offtake agreements with Eskom.

The 68 MW LSP project at Grootegeluk Mine reached financial close on 29 June 2023 under a 25-year Power Purchase Agreement with Exxaro Coal Proprietary Limited.

Construction commenced during the second half of 2023 and commercial operation is expected in early 2025.

Cennergi's operating wind assets project financing of R 4 348 million (2022: R4 554 million) will mature and be fully settled by the end of 2031. Cennergi's solar assets project financing will mature and be fully settled by the end of 2042. The project financing has no recourse to the Exxaro balance sheet and is hedged through interest rate swaps.

Equity-accounted income from SIOC increased by 51% to R6 157 million (2022: R4 077 million), driven by higher iron ore prices and sales volumes, as well as cost optimisation initiatives and as a result of the prior year including an impairment charge recognised on mining assets.

An interim dividend of R1 967 million was received from the investment in SIOC in August 2023. SIOC declared a final dividend to its shareholders in February 2024. Exxaro's share of the dividend amounts to R2 107 million, which is 7% higher than the interim dividend received. The dividend will be accounted for in the first half of 2024.

As part of the broader Exxaro strategic review, the company continuously seeks opportunities to unlock value to support its Sustainable Growth and Impact strategy. As previously reported, Exxaro has identified that the FerroAlloys business is no longer a strategic fit within the envisaged minerals business portfolio and a sales process has commenced to dispose of the entire shareholding in Exxaro FerroAlloys Proprietary Limited. Exxaro aims to enhance the economic participation of Black-owned companies in the South African economy. In line with this intent, Exxaro has earmarked the FerroAlloys disposal process to target Black ownership.

The sales process is still in the initial stages and therefore the FerroAlloys business did not meet all the criteria in terms of IFRS 5 Non-current Assets Held for Sale and Discontinued Operations to be classified as a non-current asset held-for-sale on 31 December 2023.

The current B-BBEE scorecard reflects a recognition Level 2. The 2023 audit is still in progress and the certificate will be published as soon as the audit is concluded.

Exxaro's decarbonisation strategy aims for an integrated, multi-stakeholder approach to position the business for a resilient and sustainable future. Exxaro realises that it cannot act alone to achieve its carbon neutrality objective by 2050, Scope 3 emission reductions and ESG objectives. In the fourth quarter of 2023, a strategic partnership with the Council of Geoscience was formed with the intent to collaborate on carbon capture, utilisation, and storage (CCUS), a technology which is key in reducing greenhouse gas emissions. Developments in the CCUS space are a critical consideration in our decarbonisation strategy.

With regards to the draft decarbonisation roadmap, Exxaro refined inputs based on internal stakeholder comments and are currently addressing the costs associated with the implementation of the roadmap.

Social investments at 31 December 2023 amounted to R1 897 million (2022: R 1 620 million), building on the 2022 trend and commitment to creating socio-economic impact in host communities. The local procurement spend on Black SMME's constitutes 71% of the social investment. Combined, these initiatives supported 277 SMME's through local procurement, as well as enterprise and supplier development, and provided 29 employment opportunities through social and labour plans.

An amount of R22 million (FY22: R10 million) was invested in Youth Employment Service (YES) programmes that provide training to youth from our host communities as follows:

The group has consistently maintained that when determining the level of dividend pay-out, and therefore the dividend cover, cognisance needs to be taken of the current state of the industry, Exxaro's capital expenditure requirements and other relevant commitments.

This is particularly relevant in the challenging economic environment, including, amongst other, the impact of the logistical challenges.

The board of directors has declared a final cash dividend, comprising:

Notice was given that a gross final cash dividend, number 42 of 1 010 cents per share, for the year ended 31 December 2023 was declared from income reserves and is payable to shareholders of ordinary shares.

Given the net cash position at 31 December 2023 of R14 834 million (excluding energy's net debt), in addition to the final dividend declared, the board of directors has resolved to pay a special dividend of 572 cents per share (approximately R2 billion) from income reserves. The special dividend is subject to SARB approval, which was obtained on 3 April 2024.

For details of the final and special dividends, refer note 5.5.

Salient dates for payment of the final and special dividends are:

| Finalisation date for the special dividend | Thursday, 4 April 2024 |

| Last day to trade cum dividend on the JSE | Tuesday, 7 May 2024 |

| First trading day ex dividend on the JSE | Wednesday, 8 May 2024 |

| Record date | Friday, 10 May 2024 |

| Payment date | Monday, 13 May 2024 |