Exxaro Resource limited Report Selector 2018

Currently viewing Annual Financial Report 2018

Currently viewing Annual Financial Report 2018

Exxaro Resources Limited Group and company annual financial statements

The group’s net operating profit from continuing operations for 2018 increased by R4 728 million to R5 703 million (2017: R975 million). The coal business benefited from higher revenue from the commercial mines, an increase in Eskom sales volumes and higher exports while the group’s results were impacted by various key transactions, including costs associated with the implementation of the Replacement BEE Transaction in 2017 of R4 339 million.

Income from equity-accounted investments (continuing and discontinued) of R3 259 million for 2018 (2017: R2 123 million) increased by 54%. This is as a result of key transactions which occurred in 2017, Exxaro’s share of the loss incurred by Tronox Limited on the disposal of the Alkali chemicals business of R1 271 million which was partly offset by an impairment reversal of property, plant and equipment (R716 million net of tax) from SIOC. In 2018, Tronox SA reported improved operating performance and foreign currency exchange gains. In addition, Cennergi’s financial results were boosted by fair value adjustments on derivative instruments and a change in the useful life of property, plant and equipment.

The key transactions shown below should be considered for a better understanding of the comparability of results between 2018 and 2017.

KEY TRANSACTIONS IMPACTING ON COMPARABILITY

| Reporting segment | Description | 2018 Rm |

2017 Rm |

|||

| Coal | – | Insurance claim received from external parties1 | 57 | 3 | ||

|---|---|---|---|---|---|---|

| – | Gain on disposal of non–core investments1,2 | 171 | ||||

| – | Gain/(loss) on disposal of property, plant and equipment1,3 | 121 | (62) | |||

| – | Post–tax share of equity–accounted investments' remeasurements1 | (1) | ||||

| Ferrous | – | Post–tax share of SIOC's loss on disposal of property, plant and equipment1 | (13) | (11) | ||

| – | Post–tax share of SIOC's reversal of impairment of property, plant and equipment1 | 716 | ||||

| TiO2 | – | Loss on dilution of shareholding in Tronox Limited1 | (106) | |||

| – | Gain on partial disposal of investment in Tronox Limited including the recycling of the foreign currency translation reserve, offset by a loss on the recycling of the financial instruments revaluation reserve to profit or loss1 | 5 191 | ||||

| – | Post–tax share of Tronox's gain on disposal of property, plant and equipment1 | 1 | 1 | |||

| – | Post–tax share of Tronox Limited's loss on disposal of Alkali chemical business1 | (1 271) | ||||

| Energy | – | Post–tax share of Cennergi's net gain on disposal of property, plant and equipment1 | 1 | |||

| Other | – | Loss on disposal of financial asset | (2) | |||

| – | Receivable relating to the disposal of the Mayoko iron ore project written off | (27) | ||||

| – | BEE credentials expense and transaction costs | (4 339) | ||||

| – | Fair value adjustment on contingent consideration relating to the acquisition of ECC | (357) | (354) | |||

| Loss on disposal of property, plant and equipment1 | (2) | |||||

| – | Recycling of the foreign currency translation reserve on liquidation of foreign entities to profit or loss1 | 14 | (58) | |||

| Net financing cost | – | Eyesizwe preference dividend accrued (consolidation impact) | (100) | (11) | ||

| Net tax adjustments | – | Tax on key transactions | (29) | 17 | ||

| Group | Total attributable earnings impact | (137) | (313) | |||

1Excluded from headline earnings.

2Comprises gains on disposal of Manyeka (R69 million) and of certain assets and liabilities of NBC (R102 million).

3Includes R115 million gain on disposal of mineral properties by Matla.

REVENUE

Group revenue increased by 12% to R25 491 million (2017: R22 813 million), mainly due to higher coal selling prices and higher Eskom commercial volumes at Grootegeluk, based on demand from Medupi power station, partially offset by a lower quality product mix. The average price per tonne achieved on exports was US$77 (2017: US$69). The average spot exchange rate realised was marginally stronger at R13.24 to the US dollar (2017: R13.30).

EARNINGS

Earnings, which include Exxaro’s share of equity-accounted investments was R7 030 million (2017: R5 982 million) or 2 801 cents per share (2017: 1 923 cents per share), impacted by various key transactions (as shown in the table above).

Headline earnings increased to R6 707 million (2017: R1 560 million) or 2 672 cents per share (2017: 502 cents per share), driven by the following non-recurring costs in the prior year:

Below is a summary of the earnings from equity-accounted investments:

| Equity-accounted income/(loss) | Dividends received | ||||||||

| 2018 Rm |

2017 Rm |

2018 Rm |

2017 Rm |

||||||

| Mafube | 114 | 259 | |||||||

|---|---|---|---|---|---|---|---|---|---|

| RBCT | (36) | (24) | |||||||

| SIOC | 2 592 | 3 303 | 2 569 | 1 390 | |||||

| Tronox SA | 382 | 67 | |||||||

| Tronox UK1 | 110 | 119 | |||||||

| Tronox Limited2 | (1 829) | 69 | 109 | ||||||

| Cennergi | 66 | 2 | 58 | ||||||

| LightApp3 | (5) | ||||||||

| AgriProtein4 | (31) | ||||||||

| Black Mountain | 70 | 226 | |||||||

| Curapipe | (3) | ||||||||

| Total | 3 259 | 2 123 | 2 696 | 1 499 | |||||

1Application of the equity method of accounting ceased when the Tronox UK investment was classified as a non-current asset held-for-sale on 30 November 2018.

2Application of the equity method of accounting ceased when the Tronox Limited investment was classified as a non-current asset held-for-sale on 30 September 2017.

3Acquired on 18 September 2018.

4Acquired on 31 May 2018.

CASH FLOW AND FUNDING

Cash flow generated by operations of R7 024 million (2017: R6 826 million) plus dividends received from investments in associates and joint ventures of R2 696 million was sufficient to cover capital expenditure and ordinary dividends as shown below.

| Deploying cash generated by operations | 2018 Rm |

2017 Rm |

||

| Cash generated by operations | 7 024 | 6 826 | ||

|---|---|---|---|---|

| Dividends received from investments in associates and joint ventures | 2 696 | 1 499 | ||

| Net finance costs | (289) | (409) | ||

| Capital expenditure | (5 790) | (3 921) | ||

| Tax paid | (1 007) | (790) | ||

| Final/interim ordinary dividend paid | (2 334) | (2 227) | ||

| Net surplus | 300 | 978 |

Total capital expenditure increased by R1 869 million mainly due to investments in the GG6 phase 2 expansion and Belfast projects.

SIOC declared a final dividend to shareholders on 14 February 2019, totalling R1 369 million for Exxaro’s 20.62% shareholding. This dividend will be recognised as part of the 2019 interim results.

DEBT EXPOSURE

The group had net debt of R3 867 million at 31 December 2018 compared to net cash of R69 million at 31 December 2017.

Net debt includes the preference share liability of R609 million (2017: R2 478 million) for Eyesizwe.

In addition to cash flow items noted above, a gross special dividend of R4 502 million (R3 149 million paid to external shareholders) was paid to shareholders on 5 March 2018 after the partial disposal of the shareholding in Tronox Limited in October 2017.

Trading conditions in the domestic market were strong in 2018, resulting in all premium product being sold at stable prices. Exxaro's supply to Eskom increased in line with contractual commitments while all other markets remained stable.

The international export market recorded strong demand for most of 2018. India increased its demand for South African lower-grade material up to the third quarter of 2018, when the market became oversupplied with coal from Indonesia and Australia after the ban on coal imports by China. Demand from South Korea slowed in 2018 as South African coal could not compete with Colombian material, but new opportunities came from Japan after Exxaro shipped a trial cargo to a power plant and received a new order for 2019. In Pakistan, new coal-fired power plants were commissioned in 2018, increasing annual coal demand to 6Mtpa from the traditional 4Mtpa. Exxaro made further inroads into the Pakistan market, supplying both the power plant and cement industries.

China has recently relaxed the ban on coal imports. However, there is still a strong indication that it will continue to protect its domestic market by limiting coal imports. If China imposes a further ban on imports, this will have a negative impact on coal pricing, especially into India.

In addition to favourable domestic and international trading conditions, Exxaro realised year-on-year operational excellence improvements and successfully implemented two key initiatives, namely visualisation of Exxaro's mining value chain and the integrated operations centre at some of Exxaro's major mines, focused on eliminating systemic waste.

REVENUE

Coal revenue increased by 12% to R25 302 million (2017: R22 553 million). Higher revenue from the commercial mines reflects higher selling prices, an increase in Eskom sales volumes and higher export sales. This was partially offset by lower domestic sales and a lower product quality mix.

CAPEX AND PROJECTS

Exxaro's capital for its coal business increased by 50% compared to 2017. This is mainly due to:

The higher capex is partly offset by:

| Coal capex | 2018 Rm |

2017 Rm |

Change % |

|||

| Sustaining | 2 779 | 3 203 | -13 | |||

|---|---|---|---|---|---|---|

| Commercial: Waterberg | 1 904 | 2 687 | -29 | |||

| Commercial: Mpumalanga | 875 | 516 | +70 | |||

| Expansion | 2 943 | 601 | ||||

| Commercial: Waterberg | 1 987 | 440 | ||||

| Commercial: Mpumalanga | 956 | 161 | ||||

| Total coal capex | 5 722 | 3 804 | +50 |

EQUITY-ACCOUNTED INVESTMENT

Mafube, a 50% joint venture with Anglo, recorded lower equity-accounted income of R114 million (2017: R259 million), mainly due to ramping down at Springboklaagte and ramping up at the Nooitgedacht reserve.

EQUITY-ACCOUNTED INVESTMENTS

Equity-accounted income from SIOC was R2 592 million (2017: R3 303 million). The lower equity-accounted income is mainly attributable to Exxaro’s share of a post-tax impairment reversal of R716 million for property, plant and equipment during 2017. An interim dividend of R1 263 million was received from SIOC in 2018 (2017: R1 390 million). A final dividend, of which Exxaro’s share will be R1 369 million, was declared on 14 February 2019.

EQUITY-ACCOUNTED INVESTMENTS

Equity-accounted income from Tronox SA and Tronox UK increased by R306 million to R492 million compared to 2017. This is mainly due to improved operating performance and foreign currency exchange gains.

Exxaro is committed to monetising the remaining 23.35% interest in Tronox Limited to focus on core activities, repay debt, fund capital commitments and make distributions to shareholders by applying the capital allocation framework. In this regard, on 26 November 2018, Exxaro and Tronox Limited agreed to address the following key matters:

The investment in Tronox Limited continues to meet the criteria to be classified as a non-current asset held-for-sale. In addition, Exxaro's membership interest in Tronox UK was classified as a non-current asset held-for-sale as of 30 November 2018, when all the requirements in terms of IFRS 5 Non-current Assets Held-for-sale and Discontinued Operations were met, and application of the equity method ceased.

On 15 February 2019, Tronox Limited confirmed the completion of the first stage of its redomiciliation, in which it has acquired Exxaro's 26% ownership interest in Tronox UK for R2.1 billion.

On 8 March 2019, Tronox Limited announced that the shareholders of Tronox Limited approved the transaction to redomicile to the United Kingdom from Australia.

EQUITY-ACCOUNTED INVESTMENTS — CENNERGI

Equity-accounted income from Cennergi, a 50% joint venture with Tata Power, increased from R2 million in 2017 to R66 million in 2018. Financial results were boosted by fair value adjustments on derivative instruments, as well as a change in the useful life (from 20 years to 30 years) of property, plant and equipment at the two wind farms which reduced the depreciation charge.

In 2018, Exxaro received dividends of R58 million as well as R186 million for the settlement of shareholder loans.

EQUITY-ACCOUNTED INVESTMENTS — OTHER

On 31 May 2018, Exxaro acquired an equity interest in AgriProtein. The purchase price of US$52.5 million comprises initial cash of US$14.5 million (R184.2 million) paid on 1 June 2018 and a deferred consideration of US$38 million (R482.8 million), which will be paid over the next two years. The timing of the deferred consideration depends on AgriProtein’s capital expenditure requirements. Transaction costs of R6.6 million were capitalised to the cost of the investment. AgriProtein develops municipal organic waste-conversion plants to generate high-quality, natural protein sold for use in animal feed and agriculture.

On 18 September 2018, Exxaro acquired an equity interest in LightApp. The purchase price of US$10 million comprises initial cash of US$5 million (R71.9 million), paid on 27 September 2018, and a deferred consideration of US$5 million (R70.7 million) which will be paid over the next two years. Transaction costs of R0.6 million were capitalised to the cost of the investment. LightApp is one of the leading start-ups in industrial energy analytics. It is a software company that develops and deploys an energy management system for industrial customers. The LightApp solution enables continuous collection and analysis of energy consumption data together with production indicators from sensors on the production floor. This analysis leads to improved energy management and efficiency through deeper insights and alerts. While LightApp is a global business, Exxaro will also use the LightApp platform to improve energy management at its own operations, with the first deployment already commencing at the FerroAlloys facility in Pretoria.

To optimise Exxaro’s coal portfolio, Exxaro concluded a sale of shares agreement with Universal Coal for the 100% shareholding in Manyeka, including the 51% interest in Eloff. The transaction closed on 31 July 2018. Exxaro received net cash of R75 million, resulting in a gain on disposal of R69 million.

On 2 March 2018, Exxaro concluded a sale of asset agreement with North Block Complex Proprietary Limited to dispose of certain assets and liabilities of NBC. Given the composition of the assets, two section 11 applications were submitted to the DMR to transfer the mineral rights. Although the section 11 for the Paardeplaats mining right has not yet been granted, it was agreed with the buyer to close the transaction on 31 October 2018. Exxaro received proceeds of R17 million for the Glisa and Eerstelingsfontein reserves, resulting in a gain on disposal of R102 million.

The sale of Paardeplaats will be concluded once the section 11 approval has been obtained.

Given Exxaro’s strong balance sheet, underpinned by strong cash flow generation, the board of directors approved a revised dividend policy during 2018. The revised dividend policy comprises the following two components;

Additionally, Exxaro is targeting a gearing ratio of below 1.5 times net debt to EBITDA.

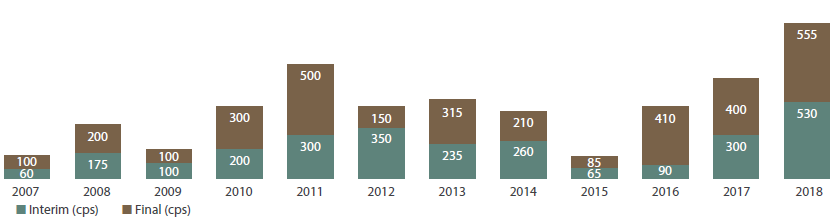

As such, Exxaro was able to declare a final dividend of 555 cents per share for 2018, bringing the total dividend for 2018 to 1 085 cents per share. Including the special dividend of 1 255 cents per share paid during 2018, total dividends during 2018 were 2 340 cents per share.

| Historical dividend declarations |

|

Exxaro expects sustainable improvement in the physical operating results for the coal business by embedding Exxaro's business optimisation and operational excellence initiatives across all operations, and unlocking value through data analytics and value-chain integration.

Exxaro is proud to report that the group is on track and within budget to deliver value on Exxaro's coal capital projects. The Belfast and Leeuwpan Lifex projects are ahead of schedule, while the GG6 expansion and Grootegeluk rapid load out station projects are impacted by community and labour related activities in the Lephalale area. Exxaro continues to engage with contractors faced with labour unrest and corporate uncertainty.

A stable domestic market is anticipated for the first half of 2019, supported by healthy prices due to tight supply in premium quality sized coal.

In Mpumalanga Eskom has, due to the termination of several coal supply agreements, requested industry participants for expressions of interest to supply coal on a short-term basis while it is looking to enter into longer-term contracts. This is positive for Exxaro as it provides more flexibility between various markets.

Exxaro remains positive that the outcome of the national elections on 8 May 2019 will put South Africa on a renewed investment and economic growth path urgently needed to address the socio-economic challenges the country is facing. Exxaro is fully supportive of the investment drive spearheaded by the Presidency.

The international market remains largely bearish owing to possible market oversupply, which hinges on China and its ban on coal imports. An increase in coal demand is expected in India, a market that is likely to remain Exxaro's main export destination.

Market conditions are expected to be supportive in 2019. Exxaro will continue to explore more opportunities in emerging markets where coal-fired power plants are being commissioned.

During the first half of 2019, the performance of the SIOC investment will be boosted by higher iron ore prices after supply disruptions in Brazil, a relative high global lump premium and a weak rand/US dollar exchange rate.

Although global economic activity is edging down and market sentiment is challenging, commodity price support in the second half of 2018 is expected to continue into the first half of 2019. However, global policy tensions, especially on trade, remain the biggest threat to global growth. The rand/US dollar exchange rate is expected to remain volatile during the period.

1 Opinions expressed herein are by nature subjective to known and unknown risks uncertainties. Changing information or circumstances may cause the actual results, plans and objectives of Exxaro Resources Limited (the company) to differ materially from those expressed or implied in the forward-looking statements. Financial forecasts and data given herein are estimates based on the reports prepared by experts who in turn relied on management estimates. Undue reliance should not be placed on such opinions, forecasts or data. No representation is made as to the completeness or correctness of the opinions, forecasts or data contained herein. Neither the company, nor any of its affiliates, advisers or representatives accept any responsibility for any loss arising from the use of any opinion expressed or forecast or data herein. Forward looking statements apply only as of the date on which they are made and the company does not undertake any obligation to publicly update or revise any of its opinions or forward looking statements whether to reflect new data or future events or circumstances.