Exxaro Resources Limited

Integrated report for the year ended 31 December 2025

Operational excellence and ongoing investment in our manufactured capital drives strategy execution and enhances the resilience of our business model.

Exxaro's manufactured capital comprises the physical mining, energy and property assets we use to deliver our products. The quality of these assets and how effectively we use them impact our operational performance and overall value creation.

We invest in our assets to preserve their long-term value and ensure reliable performance, while optimising their use to deliver high-quality products. Portfolio optimisation, together with effectively using our invested capital, support value creation and preservation across the other five capitals.

| Material theme | Matters | Strategies to achieve our objectives | Related strategic objectives | Our broader impact | ||

|

Adapting to a changing context |

|

|

||||

|

Executing our strategy |

|

|

|

Coal

Delivered coal to customers effectively and efficiently through continuous process improvements, strengthening operational performance while optimising value across the value chain.

Metals

Received dividends amounting to R3.3 billion from our investment in SIOC. SIOC and Black Mountain also achieved a year-on-year increase in adjusted equity-accounted income.

Energy solutions business

Announced the acquisition of majority interests in two operational renewable energy assets, which will contribute an additional 213MW of generation capacity to Cennergi's portfolio once the transaction is finalised in 2026. Cennergi was also awarded preferred bidder for the 240MW Corona solar project.

In May 2025, Exxaro announced the acquisition of select manganese assets in the Kalahari Manganese Field in the Northern Cape. Manganese is essential in steelmaking and is increasingly important in battery and renewable energy technologies, making it a key mineral in South Africa’s industrial and energy transition. The acquisition aligns directly with our Sustainable Growth and Impact strategy by diversifying earnings, reducing reliance on coal and positioning the business to participate in long-term growth markets linked to the global energy transition. The transaction was concluded post-year end.

Looking

ahead

Exxaro’s coal and metals business approach supports the transition to a low-carbon world while leveraging our core mining and logistics competencies. Guided by comprehensive screening criteria, we identify key energy transition metals that position us for future growth.

In parallel, we focus on enhancing our ability to fulfil current energy demands. Our market-to-resource optimisation strategy incorporates market insights and dynamics into operational and strategic planning to produce coal products that meet customers’ requirements and changing market demands.

By integrating these strategies, we balance optimal performance with advancing our growth ambitions.

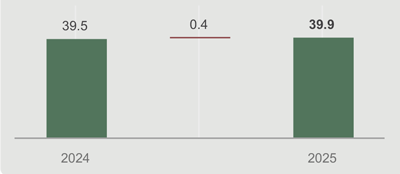

Total product (Mt)

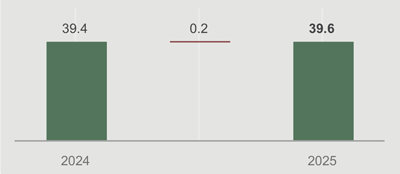

Total sales (Mt)

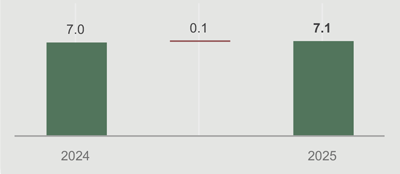

Export sales (Mt)

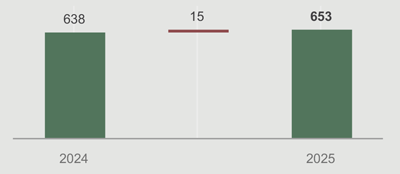

Cash cost per total tonnes handled (R/t)

Total cash cost per production tonne (R/t)

International thermal coal pricing (API4) averaged US$90/t in 2025 (2024: US$105/t). Prices declined from 2024 levels, as the coal market remained well supplied through the year. Other drivers included stable stock levels in South Africa’s key markets, lower gas pricing, growth in renewables and increased nuclear energy generation.

In line with our market-to-resource optimisation strategy, production was aligned to market demand. The business was mainly impacted by lower demand from Eskom. Export sales performed well, with an increase of 2% from 2024.

Our continuous cost optimisation focus delivered results and will remain a pivotal element in achieving operational efficiencies, ensuring resources are utilised effectively and that performance aligns with our goals.

Total cash cost in absolute terms increased by 0.04% year on year, delivering on our improvement and efficiency projects and absorbing mining inflation currently at 1.1%.

In absolute cash cost terms, we experienced cost savings on all levels, except on employee cost due to filling of vacancies and annual salary increases, a once-off credit in the second half of 2024, which did not recur in 2025, and increased service level costs.

Total cash cost per tonne was impacted by lower volume offtake from Eskom.

Total volumes handled decreased in line with the expected mining geographical landscape from the various operations, resulting in an increased cash cost per total tonnes handled.

EBITDA remained stable despite a 14% decline in the API4 price, supported by lower operating costs.

In the context of a challenging macro-economic environment, we are strengthening business resilience through disciplined cost optimisation and efficiency gains across the value chain, positioning the business for sustained, consistent performance.

SIOC’s adjusted equity-accounted income increased to R3 989 million (2024: R3 383 million), mainly due to higher realised iron ore prices and improved operational stability across the value chain. In July 2025, Exxaro received an interim dividend of R1 535 million from SIOC. In February 2026, SIOC declared a final dividend of R1 344 million to Exxaro.

Adjusted equity-accounted income from Black Mountain increased to R490 million (2024: R65 million), driven by higher zinc production and sales volumes resulting from more favourable mining conditions, partially offset by lower commodity prices relative to 2024.