Integrated report 2019

Exxaro Resources Limited

Group and company annual financial statements

for the year ended 31 December 2019

The group’s net operating profit (from continuing and discontinued operations) for 2019 increased by R696 million to R6 399 million (2018: R5 703 million) mainly due to the net gain on the partial disposal in Tronox Holdings plc and the redemption of Exxaro’s membership interest in Tronox UK.

Income from equity-accounted investments of R4 693 million for 2019 (2018: R3 259 million) increased by 44%, mainly as a result of SIOC.

The key transactions shown below should be considered for a better understanding of the comparability of results between 2019 and 2018. Please note that when we present our figures to the market we do this on a normalised basis, taking into account the key transactions impacting comparability, as shown in the table below:

Table 1: Key transactions impacting comparability

| Reporting segment | Description | 2019 Rm |

2018 Rm |

|||

| Coal | – | Insurance claim recovery from external parties | (99) | |||

|---|---|---|---|---|---|---|

| – | Targeted voluntary packages1 | 393 | ||||

| – | Insurance claim recovery from external parties2 | (49) | (57) | |||

| – | Gain on disposal of non-core investments2, 3 | (76) | (171) | |||

| – | Loss on loss of control of Tumelo2 | 35 | ||||

| – | Net gains on disposal of property, plant and equipment2, 4 | (18) | (121) | |||

| – | Impairment reversal of property, plant and equipment2 | (23) | ||||

| – | Tax on non-core adjustments2 | 11 | 29 | |||

| Ferrous | – | Targeted voluntary packages1 | 3 | |||

| – | Post-tax share of SIOC’s loss on disposal of property, plant and equipment2 | 10 | 13 | |||

| TiO2 | – | Indemnification asset movement relating to the tax implications of the partial Tronox Holdings plc divestment | (65) | |||

| – | Net gains on partial disposal of investment in Tronox, including net gain on translation differences recycled to profit or loss2, 5 | (2 336) | ||||

| – | Tax on partial disposal of investment in Tronox Holdings plc2 | 65 | ||||

| Energy | – | Impairment of associate (GAM)2 | 58 | |||

| Other | – | Fair value adjustment on debt | (58) | |||

| – | Fair value adjustment on the ECC contingent consideration | (296) | 357 | |||

| – | Net gain on translation differences recycled to profit or loss on foreign subsidiaries2 | (7) | (14) | |||

| – | Net loss on disposal of property, plant and equipment2 | 18 | ||||

| – | Losses on dilution of investments in associates2 | 42 | ||||

| – | Post-tax share of Insect Technology’s loss on disposal of intangible assets and impairment of goodwill2 | 42 | ||||

| Various | – | Other items individually less than R10 million2 | 4 | 1 | ||

| Net financing cost | – | Eyesizwe preference dividend accrued (consolidation impact) | 25 | 100 | ||

| Non-controlling interest | – | NCI on non-core adjustments | (86) | |||

| Group | Total attributable earnings impact | (2 407) | 137 |

| 1 | Exxaro is committed to complying with the employment equity targets prescribed by the Mining Charter and Department of Trade and Industry codes and as such approved various mechanisms that will support the achievement of the 2022 targets. |

| 2 | Excluded from headline earnings. |

| 3 | Relates to a gain on disposal of the Paardeplaats mining right. 2018 comprises a gain on disposal of Manyeka (R69 million) and a gain on disposal of NBC (R102 million). |

| 4 | 2018 includes a R115 million gain on disposal of mineral properties by Matla. |

| 5 | Includes a gain of R1 234 million on the partial disposal of Tronox Holdings plc, a gain of R832 million on translation differences recycled to profit or loss on partial disposal of Tronox Holdings plc and a gain of R270 million on the redemption of the Tronox UK membership interest. |

Group revenue increased by 1% to R25 726 million (2018: R25 491 million). While coal export volumes increased by 14%, there was a significant decline in the API4 price resulting in a 30% lower average price per tonne achieved of US$54 (2018: US$77). The negative impact was cushioned somewhat by a weaker average spot exchange rate of R14.44 to the US dollar (2018: R13.24). On the domestic front, higher prices from commercial mines had a positive revenue impact.

Earnings of R9 809 million (2018: R7 030 million) or 3 908 cents per share (2018: 2 801 cents per share), were impacted by various once-off transactions (+ as shown in Table 1 above).

Headline earnings increased to R7 599 million (2018: R6 707 million) or 3 027 cents per share (2018: 2 672 cents per share). This was mainly driven by an increase of R1 434 million in Exxaro’s share of income of equity-accounted investments to R4 693 million (2018: R3 259 million), which more than offset the drop in coal earnings.

Below is a summary of the earnings from equity-accounted investments:

| Equity-accounted income/(loss) |

Dividends received |

|||||||

| 2019 Rm |

2018 Rm |

2019 Rm |

2018 Rm |

|||||

| SIOC | 4 413 | 2 592 | 4 051 | 2 569 | ||||

|---|---|---|---|---|---|---|---|---|

| Tronox SA | 234 | 382 | ||||||

| Tronox UK1 | 110 | 50 | ||||||

| RBCT | 1 | (36) | ||||||

| Curapipe | (4) | (3) | ||||||

| Insect Technology | (148) | (31) | ||||||

| LightApp | (28) | (5) | ||||||

| Black Mountain2 | 52 | 70 | ||||||

| Mafube | 127 | 114 | ||||||

| Cennergi | 46 | 66 | 95 | 58 | ||||

| Total | 4 693 | 3 259 | 4 196 | 2 627 | ||||

| 1 | Application of the equity method of accounting ceased when the Tronox UK investment was classified as a non-current asset held-for-sale on 30 November 2018. |

| 2 | Application of the equity method of accounting ceased when the Black Mountain investment was classified as a non-current asset held-for-sale on 30 November 2019. |

Net debt for the year ended 31 December 2019 increased by R1 943 million to R5 810 million (2018: R3 867 million). The main cash outflow items during 2019 include the funding of our capital expenditure programme of R6 076 million, R344 million cash payment in respect of the ECC contingent consideration, R678 million for the acquisition of shares in the market to settle share-based payments and R263 million being the deferred consideration paid to Insect Technology.

In addition to the cash generated by our own operations and dividends received, we also received cash of R2 057 million from Tronox UK for the redemption of Exxaro’s 26% membership interest and R2 889 million from Tronox Holdings plc for the repurchase of 14 million shares from Exxaro. Of the cash received, 65% was returned to shareholders as a special dividend of R2 251 million (to external shareholders).

The dividends received by Eyesizwe resulted in the full settlement of the preference share liability in October 2019.

In the domestic market, steam coal demand remained stable with Eskom’s demand varying due to lower offtake from the Medupi power station offset by additional offtake from Leeuwpan and ECC. AMSA’s demand varied due to fluctuations in kiln operations as well as the steel plant in Saldanha being placed on care and maintenance. Exxaro has successfully placed AMSA’s material in the market with other customers.

Overall, the thermal coal seaborne market remained in oversupply. However, price support for the API4 was evident towards the end of 2019 but the sharp increase in API4 priced South African producers out of their natural markets. The competition in our markets is intensifying, with traditional Atlantic Ocean suppliers competing aggressively. The API4 averaged US$72 per tonne compared to US$98 per tonne in 2018. Export volumes increased 14% from 8.0Mt in 2018 to 9.1Mt in 2019.

Coal revenue was 1% higher at R25 582 million (2018: R25 302 million). The higher revenue was mainly driven by an increase in domestic sales due to price escalations and new contracts, partly offset by other lower domestic volumes. Although export volumes were 14% higher than the previous year, the average realised rand price per tonne was 24% lower at R774 compared to R1 013 in 2018.

Exxaro’s coal capital expenditure of R5 817 million increased by 2% compared to R5 722 million in 2018. While our expansion capital in the Mpumalanga region increased by R1 345 million, this was partly offset by a lower capex spend of R789 million in the Waterberg region. Our sustaining capital decreased by R534 million, mainly in the Mpumalanga region.

As reported previously, first coal from our greenfield Belfast mine was produced in March 2019 and first product sales took place in May 2019. Completion of the beneficiation plant is close to commissioning with ramp up expected in the first quarter of 2020. At Mafube, ramping up of the Nooitgedacht reserve to nameplate capacity was achieved in the fourth quarter of 2019 and continues to exceed expectations.

| Coal capex | 2019 Rm |

2018 Rm |

Change % |

||

| Sustaining | 2 245 | 2 779 | -19 | ||

|---|---|---|---|---|---|

| Commercial: Waterberg | 1 753 | 1 904 | -8 | ||

| Commercial: Mpumalanga | 475 | 875 | -46 | ||

| Other | 17 | ||||

| Expansion | 3 572 | 2 943 | +21 | ||

| Commercial: Waterberg | 1 198 | 1 987 | -40 | ||

| Commercial: Mpumalanga | 2 301 | 956 | +141 | ||

| Other | 73 | ||||

| Total coal capex | 5 817 | 5 722 | +2 |

Mafube, a 50% joint venture with Anglo, recorded equity-accounted income of R127 million (2018: R114 million), mainly due to the ramping up of the Nooitgedacht reserve.

Equity-accounted income from SIOC increased by R1 821 million to R4 413 million (2018: R2 592 million). The increase is primarily driven by the effect of higher iron ore prices realised and a weaker exchange rate.

Dividends amounting to R4 051 million were received from our investment in SIOC (2018: R2 569 million). SIOC has declared a final dividend to its shareholders in February 2020. Exxaro’s 20.62% share of the dividend amounts to R1 412 million. The dividend will be accounted for in 2020.

Equity-accounted income from Tronox SA decreased by R148 million to R234 million compared to 2018. The decrease is mainly as a result of increased costs (royalties and allocated head office costs), inventory revaluation adjustments and foreign currency exchange losses.

Our investment in Tronox Holdings plc continues to meet the criteria to be classified as a non-current asset held-for-sale.

Cennergi, a 50% joint venture with Tata Power, recorded equity-accounted income of R46 million for 2019 (2018: R66 million). The results were negatively impacted by the ineffective portion of interest rate swaps and fair value adjustments on share-based payment liabilities offset by improved operational performance. Cash flow generation remains positive as Exxaro received dividends of R95 million in 2019 compared to R58 million in 2018.

Despite the loss of two turbines due to fire incidents, for a significant period of the year, generation output to date at the two wind-farms is better than planned given favourable wind conditions. The replacement turbines have been commissioned in November 2019 and are in full production.

As announced on 17 September 2019, Exxaro has concluded an agreement with Khopoli, a wholly owned subsidiary of Tata Power, to acquire Khopoli’s 50% shareholding in Cennergi for an amount of R1 550 million, subject to normal working capital adjustments. Post the conclusion of the agreement, Exxaro will have 100% ownership of Cennergi. The last condition precedent was met in March 2020 (refer note 18).

During the second half of 2019, the Exxaro board of directors approved a decision to divest from its 26% interest in Black Mountain. On 30 November 2019, the investment was classified as a non-current asset held-for-sale and the application of the equity method of accounting ceased.

On 31 January 2020, the Arnot operation was transferred to Arnot OpCo Proprietary Limited Consortium. The accounting of the transfer will be accounted for in 2020.

On 20 February 2020, Exxaro announced our intention to divest our entire interest in ECC and the Leeuwpan operations. The divestment will be executed through a formal disposal process. The proposed transaction is a category two transaction in terms of the JSE Listings Requirements and is therefore not regarded as material.

We are proud to report that Eyesizwe, our BEE shareholder, fully settled its acquisition debt in October 2019, three years earlier than anticipated. The early settlement was funded from dividends received from Exxaro. From an accounting perspective, this resulted in the outside shareholders of Eyesizwe being treated as non-controlling interests for the Exxaro group from 1 November 2019.

Furthermore, we undertook to transfer at least 10% of our 24.9% shareholding in Eyesizwe into structures for the benefit of Exxaro’s employees and communities adjacent to our operations. The transaction agreements have been concluded in the first quarter of 2020 with implementation of the employee scheme expected in April 2020, and the implementation of the community scheme dependent on the registration of the company as a public benefit organisation in terms of section 18A of the Income Tax Act.

In terms of our capital allocation framework, we will remain prudent in returning cash to shareholders, managing debt and selectively reinvesting for the growth of our business. Exxaro’s declared dividend policy is based on two components: a pass through of the SIOC dividend received and a targeted cover ratio of 2.5 times to 3.5 times core attributable coal earnings.

Additionally, Exxaro is targeting a gearing ratio below 1.5 times net debt to EBITDA.

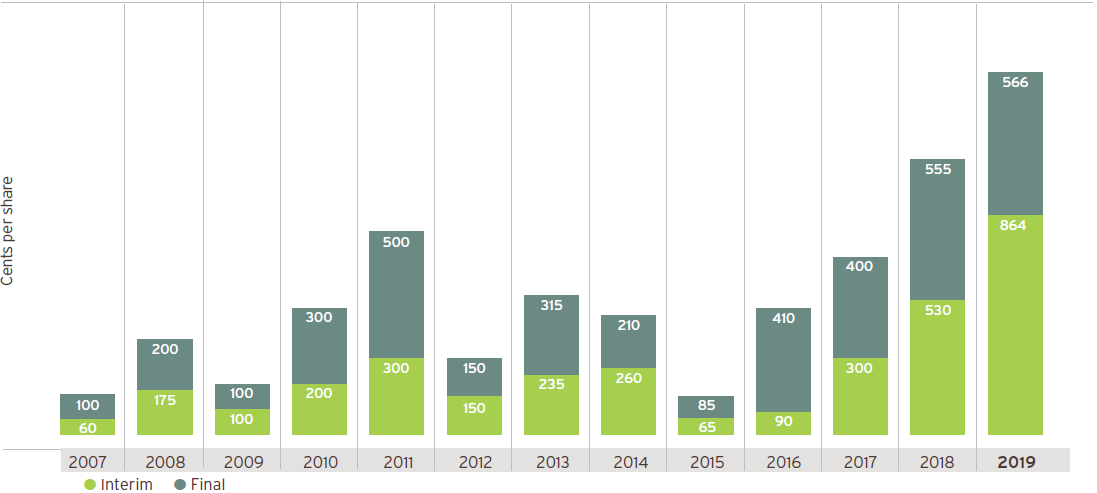

The board of directors has declared a cash dividend comprising:

As such, Exxaro declared a final dividend of 566 cents per share for 2019, bringing the total dividend declared for 2019 to 2 327 cents per share, which includes a special dividend of 897 cents per share.

| Historic dividend declarations |

|

In the first half of 2020, global economic growth stabilisation is anticipated. However, depending on the duration and spread of the coronavirus in China, recovery in thermal coal import demand in China might support the seaborne market somewhat.

We expect domestic thermal coal demand and pricing to remain relatively stable during 2020.

The API4 is expected to be under pressure as a similar liquefied natural gas (LNG) supply wave, as evident in 2019, is anticipated to continue into 2020, together with low gas prices globally.

South Africa’s fiscal imbalance is set to remain a major constraint in addressing the increasing socio-economic challenges with the risk of a sovereign rating downgrade increasing. As a result, the rand/dollar exchange rate is expected to remain volatile.

As we roll out the integrated operations centres at all our business units, in terms of our digitalisation plan, increased visualisation of the mining value chain will highlight embedded inefficiencies that will be addressed through in-time decision making related to safety, productivity and cost performance. At an enterprise level, we are on schedule to implement our integrated management platform allowing us to access strategic insights across our operations, enabling future looking value-add conversations.

The expected recovery in iron ore seaborne supply with narrowing steel margins will soften the iron ore market.

Our shareholding in Tronox Holdings plc has been reduced to approximately 14.7 million shares, representing about 10% of the total outstanding shares as at 31 December 2019. We remain committed to monetising our stake in Tronox Holdings plc over time and in the best possible manner, taking into account prevailing market conditions.

In 2017, Exxaro adopted a strategy to explore new investment opportunities based on three pillars: water security, food security and energy security. Based on our experience since then, we have now changed that strategy to focus solely on new opportunities in the energy security space. As we pursue these opportunities, our approach will continue to be measured with a view to mitigating potential risks and ensuring that the capital allocation decisions are in line with appropriate metrics.

With regard to the Moranbah South hard coking coal project, Exxaro, together with Anglo Coal, are in the process of reassessing the potential development plan for the project.

In August 2019, we reported that we would share our climate response strategy, including our progress in incorporating the recommendations from the Financial Services Board Task Force on Climate-related Financial Disclosures (TCFD), which highlight climate change transitional and physical risks confronting our business and the related financial impacts of these risks. Our climate change position statement contains details on our approach to climate change mitigation and adaptation. The document also includes our aspirational target of scope 1 and 2 carbon neutrality by 2050. We have developed climate change scenarios that take into account the 2°C world as per the recommendation of the TCFD. We will be using these scenarios to conduct a detailed analysis to quantify the financial risks and opportunities in our operations.

Subsequent to year-end and the finalisation of the financial statements, the COVID-19 (the virus) pandemic required us to support government protocols and directives to contain the spread of the virus. We have undertaken to act responsibly in preventing the further spread of the virus and therefore implemented our Crisis Management Plan (CMP) and Business Continuity Plan (BCP) across the breadth of our businesses that includes Health and Safety controls and preventative measures. Additionally, it is important to recognise the impact on the South African economy and the cumulative negative impact of the lockdown period, which commenced on midnight, 26 March 2020 and is foreseen to last longer than anticipated. We have received the necessary approval to continue with our production activities during this period, albeit at varying reduced levels in terms of volumes and people, as these activities are considered to be essential services and the necessary measures have been taken to prevent possible infections. Refer note 18.3 for more details.

| 1 | Opinions expressed herein are by nature subjective to known and unknown risks uncertainties. Changing information or circumstances may cause the actual results, plans and objectives of Exxaro to differ materially from those expressed or implied in the forward-looking statements. Financial forecasts and data given herein are estimates based on the reports prepared by experts who in turn relied on management estimates. Undue reliance should not be placed on such opinions, forecasts or data. No representation is made as to the completeness or correctness of the opinions, forecasts or data contained herein. Neither the company nor any of its affiliates, advisers or representatives accept any responsibility for any loss arising from the use of any opinion expressed or forecast or data herein. Forward-looking statements apply only as of the date on which they are made and the company does not undertake any obligation to publicly update or revise any of its opinions or forward-looking statements whether to refl ect new data or future events or circumstances. |